Mohawk Industries Reports Q3 Results

27.10.2023, 09:12aktualizacja: 27.10.2023, 09:15

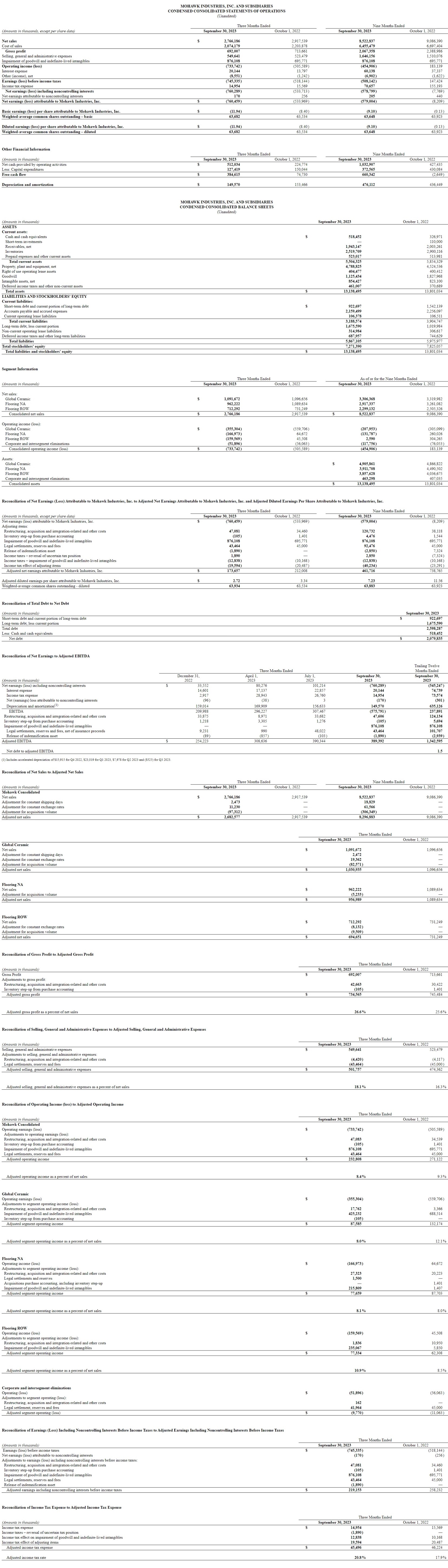

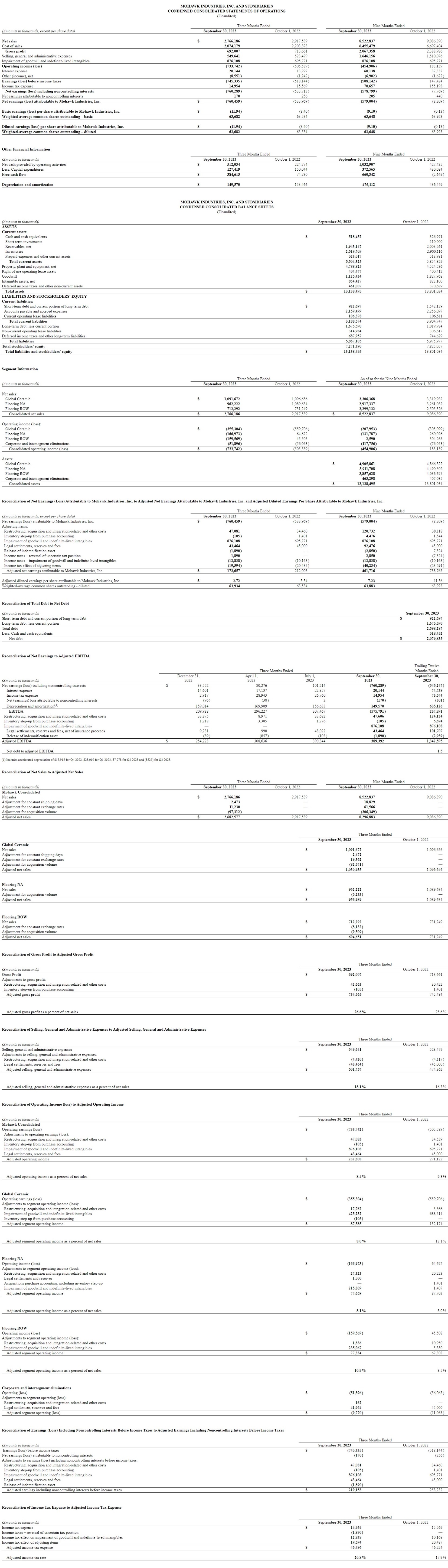

CALHOUN, Ga., Oct. 26, 2023 (GLOBE NEWSWIRE) -- Mohawk Industries, Inc. (NYSE: MHK) today announced a third quarter 2023 net loss of $760 million and a loss per share of $11.94 with the impact of non-cash impairment charges of $876 million. The Company’s current market capitalization along with continued challenging macroeconomic conditions and higher discount rates prompted a review of its goodwill and intangible asset balances, which resulted in the impairment charges. Adjusted net earnings were $174 million, and adjusted earnings per share („EPS”) were $2.72, excluding impairment and other non-recurring charges. Net sales for the third quarter of 2023 were $2.8 billion, a decrease of 5.2% as reported and 8.1% on a legacy and constant currency and days basis versus the prior year. During the third quarter of 2022, the Company reported net sales of $2.9 billion, a net loss of $534 million and a loss per share of $8.40. Adjusted net earnings were $212 million, and adjusted EPS was $3.34, excluding impairment and other non-recurring charges.

For the nine-month period ending September 30, 2023, the Company reported a net loss and loss per share of $579 million and $9.10, respectively. Adjusted net earnings were $462 million, and adjusted EPS was $7.23, excluding impairment and other non-recurring charges. For the first nine months of 2023, net sales were $8.5 billion, a decrease of 6.2% as reported and 8.7% on a legacy and constant currency and days basis versus the prior year. For the nine-month period ending October 1, 2022, the Company reported net sales of $9.1 billion, a net loss of $8 million and a loss per share of $0.13; adjusted net earnings were $739 million, and adjusted EPS was $11.56, excluding impairment and other non-recurring charges.

Commenting on the Company’s third quarter results, Chairman and CEO Jeff Lorberbaum stated, „Our results for the quarter were in line with our expectations as our industry faced continued pressures across all regions, primarily due to constrained residential investments and further tightening of consumer discretionary spending. Our third quarter performance was seasonally impacted by vacations in Europe, which reduced our sales and earnings versus the prior quarter. Lower material and energy costs offset the decline in both price and mix. We also faced foreign exchange headwinds of approximately $20 million on operating income or $0.25 on EPS. Across the business, we benefited from cost reductions, productivity initiatives and lower input costs. We are managing our working capital and generated strong free cash flow of $385 million in the quarter and $660 million for the year to date.

During the quarter, central banks around the world continued to raise interest rates to slow down their economies and reduce inflation. Their actions are affecting new construction and remodeling in both residential and commercial channels, postponing spending on new projects. In the U.S., mortgage rates have climbed to their highest level in more than two decades, which has suppressed the housing market and limited home renovation activity. In Europe, consumers are postponing large purchases like flooring as a result of higher energy costs, inflation and uncertainty due to the war in Ukraine. Our industry faces a greater impact from these pressures than other sectors given that most flooring purchases can be deferred. With the high fixed costs required to produce flooring, competition increases as the industry slows and participants attempt to increase their sales to maximize absorption. As a result, our average selling prices and mix have declined, with the impact offset by lower material and energy costs, restructuring benefits and process improvements.

The predicted timing of the housing sector recovery continues to be postponed, and we are managing the business to optimize our results and cash flow until it occurs. We are taking actions to increase our volumes while managing margins and operating expenses. We have launched differentiated collections, selectively introduced promotions and expanded our participation in the new construction channel. To further enhance our competitive position, we will shut down older ceramic production in Italy, and we are converting our U.S. rigid LVT production to a direct extrusion process. These restructuring initiatives will result in a non-recurring charge of approximately $55 million, of which $50 million is non-cash. When completed, these initiatives should improve our profitability by $30 million annually by enhancing our productivity, lowering our manufacturing costs and optimizing our production flexibility.

Our European expansions in insulation and porcelain slabs are currently in operation, and our U.S. premium laminate and LVT projects are continuing to start up. Expanded production in European laminate and U.S. quartz countertops should begin in the second half of 2024. As the integration of our acquisitions in Mexico and Brazil proceeds, we have consolidated general management, sales and administrative functions, while enhancing the companies’ product offering, operational efficiencies and customer base. While the Mexican and Brazilian markets are experiencing reduced demand and margins, we anticipate gaining additional benefits from our acquisitions as these markets recover.

For the third quarter, the Global Ceramic Segment reported a 0.5% decline in net sales as reported, or a 6.0% decline on a legacy and constant currency and days basis. The Segment’s operating margin was negative 32.5% as reported, or 8.0% on an adjusted basis, as a result of unfavorable price and product mix, temporary plant shutdowns, lower volumes and foreign exchange headwinds, partially offset by productivity gains. Our U.S. ceramic business outperformed due to our innovative product introductions and higher service levels. With this, we expanded our positions in the new home construction and commercial channels. Our investments in new decorating technology, polishing and mosaics are providing domestic alternatives to premium imported ceramic. To further expand our quartz countertop sales, we are introducing more stylized collections made utilizing new technologies that provide greater value. In Europe, retail traffic and new construction are being affected by economic uncertainty. To gain sales, we are responding with specific price promotions by geography and channel. Natural gas prices have declined more than 80% from their peak, and we have reset our pricing to align with energy costs. Sales of our premium porcelain slabs continue to grow, and we are optimizing our recent capacity expansion. In Latin America, we have reduced our cost structures to adapt to slower, more competitive markets, with Mexico being less affected. As we integrate our acquisitions, we are gaining customer commitments to expand sales across all channels and price points using the combined product portfolio.

During the third quarter, our Flooring Rest of the World Segment’s net sales decreased by 2.6% as reported, or 5.0% on a legacy and constant currency basis. The Segment’s operating margin was negative 22.4% as reported, or 10.9% on an adjusted basis, improving over prior year as it benefited from raw materials, energy and less downtime, offsetting unfavorable price, mix and foreign exchange. Sheet vinyl continues to outperform other flooring categories, and we have increased production to meet the higher demand. Our laminate and LVT sales are under pressure in the softer market, and we are introducing new products, merchandising and select promotions to optimize volumes. We have executed the restructuring to support the conversion of our residential LVT offering from flexible to rigid cores, which is positively impacting sales. Our panels business has slowed due to a decline in remodeling activity, construction projects and industrial demand. Sales of our higher margin HPL panel collections are growing as our customer base expands. Our insulation volume in the third quarter improved, and our margins were in line with last year. Insulation industry pricing has declined along with input costs, with regional variation caused by new plants coming online. In Australia and New Zealand, the industry slowed during the quarter, and our sales in both countries were down slightly. To increase sales and protect our margins, we are introducing enhanced collections across fiber categories, elevating the marketing of our high-end products and implementing targeted promotions to meet evolving demand.

In the third quarter, our Flooring North America Segment sales declined 11.7% as reported or 12.2% on a legacy basis. The Segment’s operating margin was negative 17.4% as reported, or 8.1% on an adjusted basis, as a result of unfavorable pricing and product mix, reduced volume and lower productivity due to the underutilization of plant assets, partially offset by lower inflation. Competition increased across all product categories, and, to enhance sales, we continued to invest in new products and merchandising systems to expand our retail presence. We also increased our participation in the new home construction channel with regional and national builders. We are implementing many projects to reduce costs, improve efficiencies and maximize material utilization. In residential carpet, to improve our mix, we are expanding our premium collections, which provide superior styling and features. For value conscious homeowners, we are increasing our environmentally friendly recycled polyester offering. Our sheet vinyl collections continue to perform well with budget-oriented consumers. As an alternative to PVC-based LVT products, we introduced a new resilient polymer core that is more environmentally friendly and scratch resistant. We are continuing to ramp up our West Coast LVT production and the new extrusion process in Georgia, with both expected to be substantially operational in the first quarter of 2024. We are expanding distribution of laminate in the retail and builder channels, and our new laminate collections have been well received as consumers seek premium visuals at accessible price points.

In the present industry downturn, we are managing the controllable aspects of our business while adjusting to regional market conditions. In all of our geographies, elevated interest rates and persistent inflation are restricting consumer discretionary spending, resulting in postponed remodeling projects and new home purchases. Similar pressures are beginning to reduce commercial investments as business sentiment declines. Competition for sales to utilize plant capacity is increasing in all of our markets, and lower input costs should offset the impact. With enhanced products and merchandising, selective promotions and expanding participation in the best performing sales channels, we are maximizing our volumes while managing our margins and operating expenses. Across the enterprise, we are implementing productivity, cost reduction and restructuring initiatives to lower our expenses and improve our results. We continue to manage our working capital to optimize our cash flow. We expect foreign exchange rates to continue to be an earnings headwind. Given these factors, we anticipate our fourth quarter adjusted EPS to be between $1.80 to $1.90, excluding any non-recurring charges. With this, our 2023 full year adjusted EPS should exceed $9.00.

Historically, the flooring industry undergoes greater cyclical peaks and troughs than other building products due to its postponable nature. Our business fundamentals remain strong, and we will benefit from significant pent-up demand when the industry rebounds. Given the aging U.S. housing stock, more than 80% of homeowners who responded to recent JP Morgan surveys indicated they are planning renovation projects in the near term. In addition, after years of construction trailing demand, substantial new home building will be required for many years to come. Commercial activity will expand as the economic outlook improves. As the world’s largest flooring provider, Mohawk is well positioned to capitalize on these opportunities.”

About Mohawk Industries

Mohawk Industries is the leading global flooring manufacturer that creates products to enhance residential and commercial spaces around the world. Mohawk’s vertically integrated manufacturing and distribution processes provide competitive advantages in the production of carpet, rugs, ceramic tile, laminate, wood, stone and vinyl flooring. Our industry leading innovation has yielded products and technologies that differentiate our brands in the marketplace and satisfy all remodeling and new construction requirements. Our brands are among the most recognized in the industry and include American Olean, Daltile, Durkan, Eliane, Elizabeth, Feltex, GH Commercial, Godfrey Hirst, Grupo Daltile, IVC Commercial, IVC Home, Karastan, Marazzi, Mohawk, Mohawk Group, Mohawk Home, Pergo, Quick-Step, Unilin and Vitromex. During the past decade, Mohawk has transformed its business from an American carpet manufacturer into the world’s largest flooring company with operations in Australia, Brazil, Canada, Europe, Malaysia, Mexico, New Zealand, Russia and the United States.

Certain of the statements in the immediately preceding paragraphs, particularly anticipating future performance, business prospects, growth and operating strategies and similar matters and those that include the words „could,” „should,” „believes,” „anticipates,” „expects,” and „estimates,” or similar expressions constitute „forward-looking statements”. For those statements, Mohawk claims the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995. There can be no assurance that the forward-looking statements will be accurate because they are based on many assumptions, which involve risks and uncertainties. The following important factors could cause future results to differ: changes in economic or industry conditions; competition; inflation and deflation in freight, raw material prices and other input costs; inflation and deflation in consumer markets; currency fluctuations; energy costs and supply; timing and level of capital expenditures; timing and implementation of price increases for the Company’s products; impairment charges; integration of acquisitions; international operations; introduction of new products; rationalization of operations; taxes and tax reform; product and other claims; litigation; the risks and uncertainty related to the COVID-19 pandemic; regulatory and political changes in the jurisdictions in which the Company does business; and other risks identified in Mohawk’s SEC reports and public announcements.

Conference call Friday, October 27, 2023, at 11:00 AM Eastern Time

To participate in the conference call via the Internet, please visit http://ir.mohawkind.com/events/event-details/mohawk-industries-inc-3rd-quarter-2023-earnings-call. To participate in the conference call via telephone, register in advance at https://dpregister.com/sreg/4129026795/18d03660587a8 to receive a unique personal identification number or dial 1-833-630-1962 for U.S./Canada and 1-412-317-1843 for international/local on the day of the call for operator assistance. A replay will be available until November 24, 2023, by dialing 1-877-344-7529 for U.S./Canada calls and 1-412-317-0088 for international/local calls and entering access code #9747702.

The Company supplements its condensed consolidated financial statements, which are prepared and presented in accordance with US GAAP, with certain non-GAAP financial measures. As required by the Securities and Exchange Commission rules, the tables above present a reconciliation of the Company’s non-GAAP financial measures to the most directly comparable US GAAP measure. Each of the non-GAAP measures set forth above should be considered in addition to the comparable US GAAP measure, and may not be comparable to similarly titled measures reported by other companies. The Company believes these non-GAAP measures, when reconciled to the corresponding US GAAP measure, help its investors as follows: Non-GAAP revenue measures that assist in identifying growth trends and in comparisons of revenue with prior and future periods and non-GAAP profitability measures that assist in understanding the long-term profitability trends of the Company's business and in comparisons of its profits with prior and future periods.

The Company excludes certain items from its non-GAAP revenue measures because these items can vary dramatically between periods and can obscure underlying business trends. Items excluded from the Company’s non-GAAP revenue measures include: foreign currency transactions and translation; more or fewer shipping days in a period and the impact of acquisitions.

The Company excludes certain items from its non-GAAP profitability measures because these items may not be indicative of, or are unrelated to, the Company's core operating performance. Items excluded from the Company's non-GAAP profitability measures include: restructuring, acquisition and integration-related and other costs, legal settlements, reserves and fees, net of insurance proceeds, impairment of goodwill and indefinite-lived intangibles, acquisition purchase accounting, including inventory step-up from purchase accounting, release of indemnification assets and the reversal of uncertain tax positions.

CONTACT:

James Brunk

Chief Financial Officer

(706) 624-2239

Source: GlobeNewswire

| Data publikacji | 27.10.2023, 09:12 |

| Źródło informacji | GlobeNewswire |

| Zastrzeżenie | Za materiał opublikowany w serwisie PAP MediaRoom odpowiedzialność ponosi – z zastrzeżeniem postanowień art. 42 ust. 2 ustawy prawo prasowe – jego nadawca, wskazany każdorazowo jako „źródło informacji”. Informacje podpisane źródłem „PAP MediaRoom” są opracowywane przez dziennikarzy PAP we współpracy z firmami lub instytucjami – w ramach umów na obsługę medialną. Wszystkie materiały opublikowane w serwisie PAP MediaRoom mogą być bezpłatnie wykorzystywane przez media. |

Newsletter portalu PAP MediaRoom to przesyłane do odbiorców raz dziennie zestawienie informacji prasowych, komunikatów instytucji oraz artykułów dziennikarskich, które zostały opublikowane na portalu danego dnia.

ZAPISZ SIĘ