Mohawk Industries Reports Q4 Results

09.02.2024, 12:56aktualizacja: 09.02.2024, 14:08

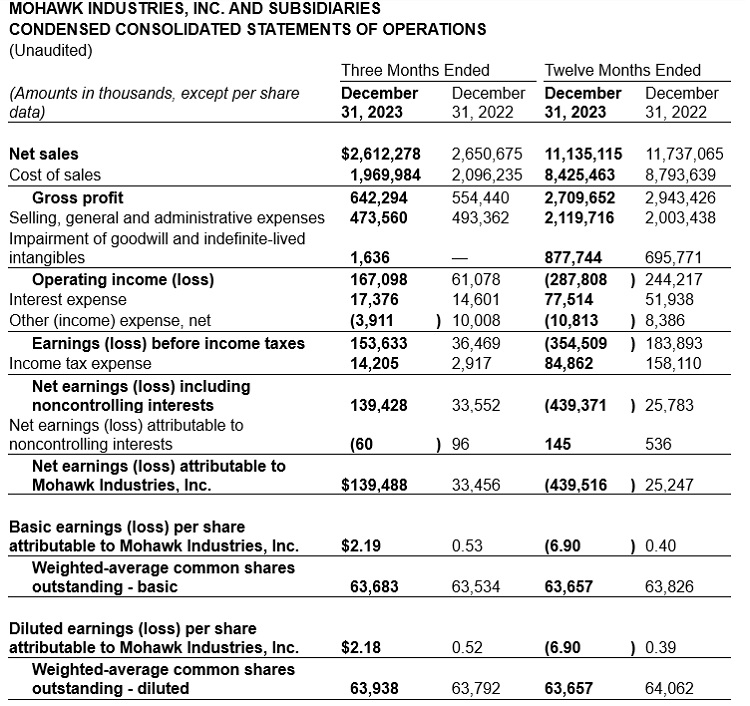

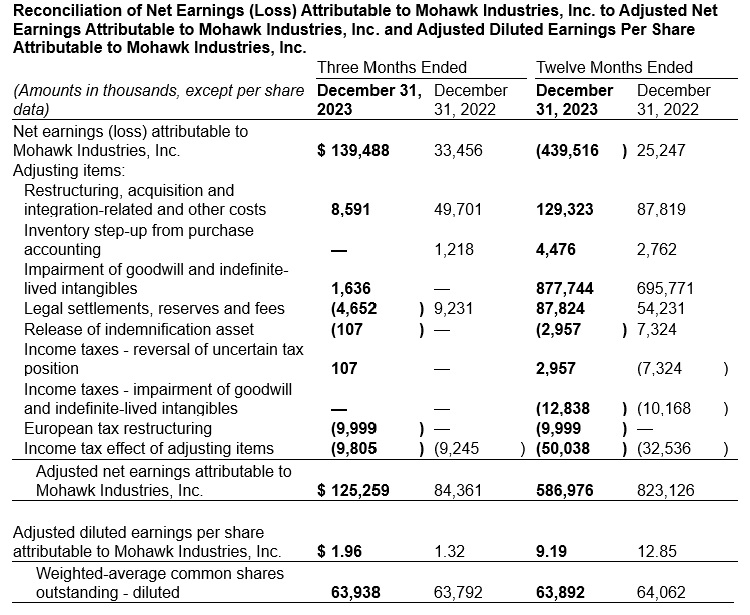

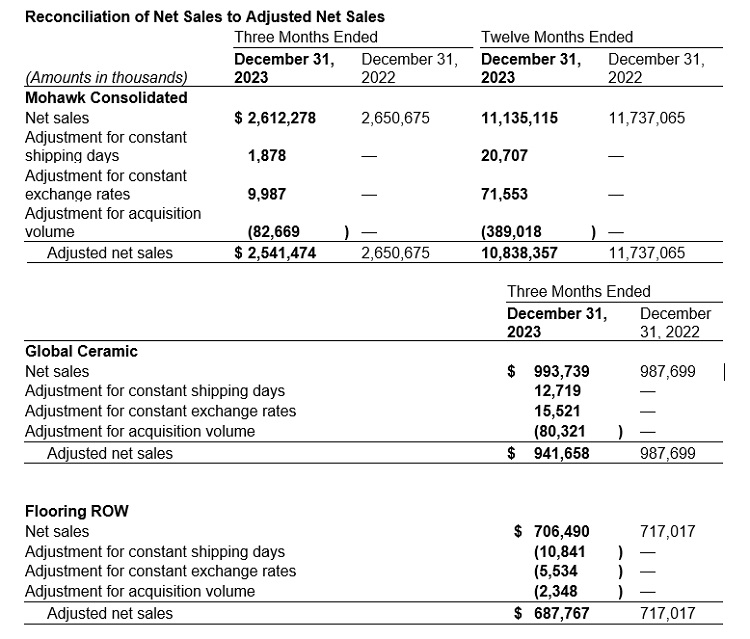

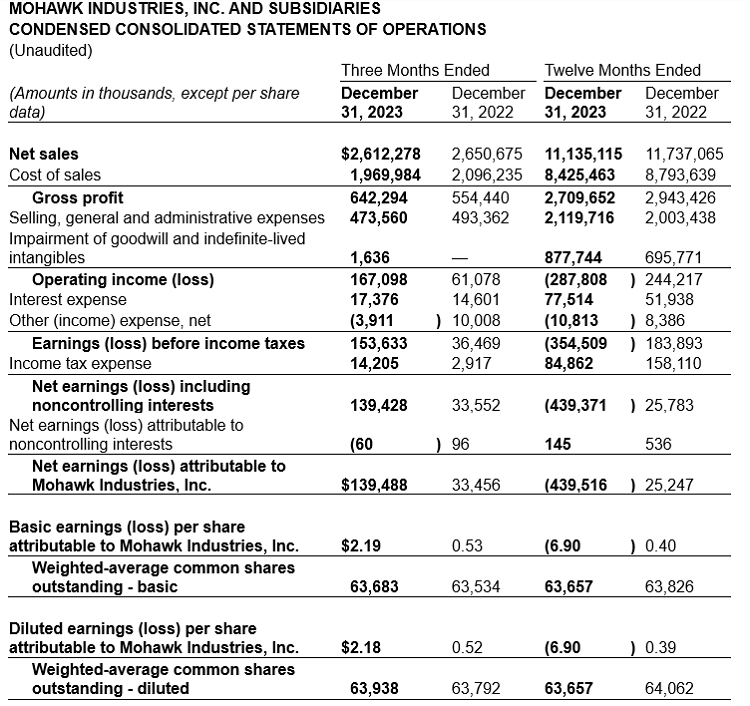

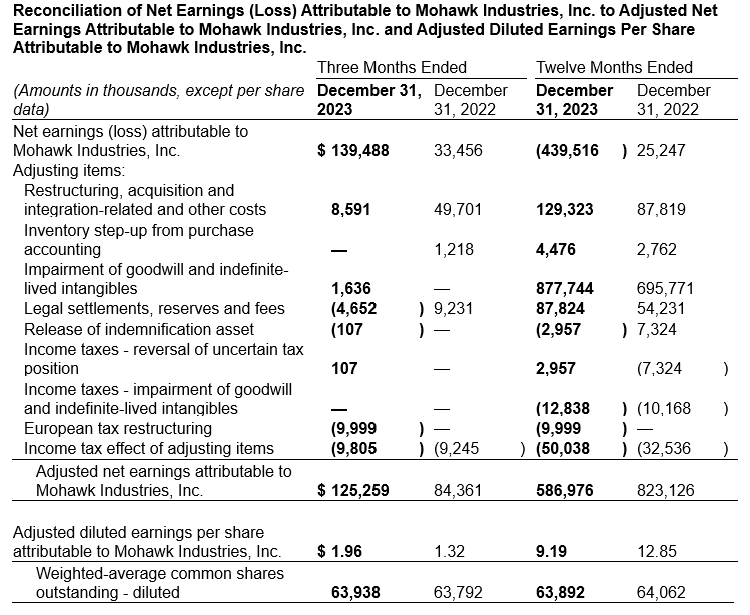

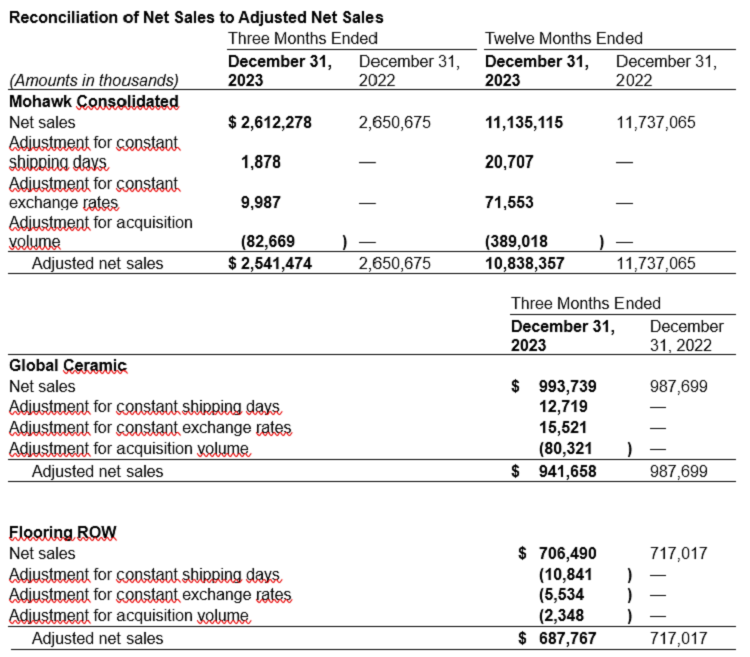

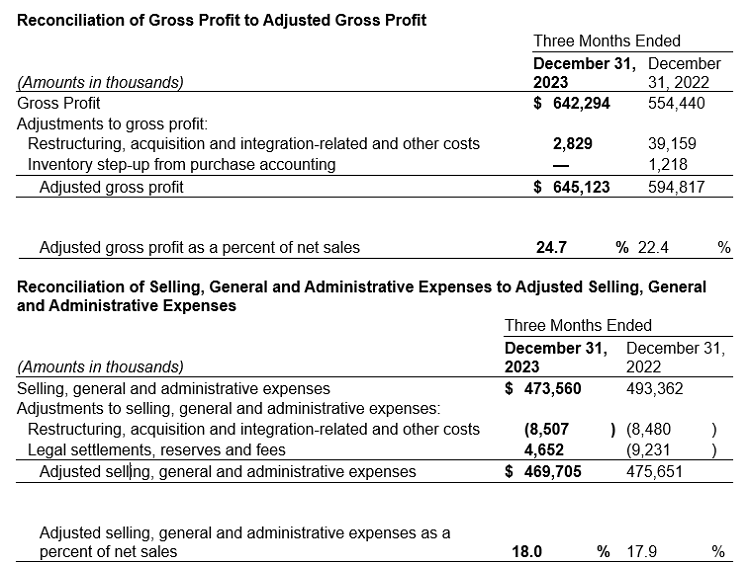

CALHOUN, Ga., Feb. 09, 2024 (GLOBE NEWSWIRE) -- Mohawk Industries, Inc. (NYSE: MHK) today announced fourth quarter 2023 net earnings of $139 million and earnings per share (“EPS”) of $2.18; adjusted net earnings were $125 million, and adjusted EPS was $1.96. Net sales for the fourth quarter of 2023 were $2.6 billion, a decrease of 1.4% as reported and 4.1% on a legacy and constant basis versus the prior year. During the fourth quarter of 2022, the Company reported net sales of $2.7 billion, net earnings of $33 million and EPS of $0.52; adjusted net earnings were $84 million, and adjusted EPS was $1.32.

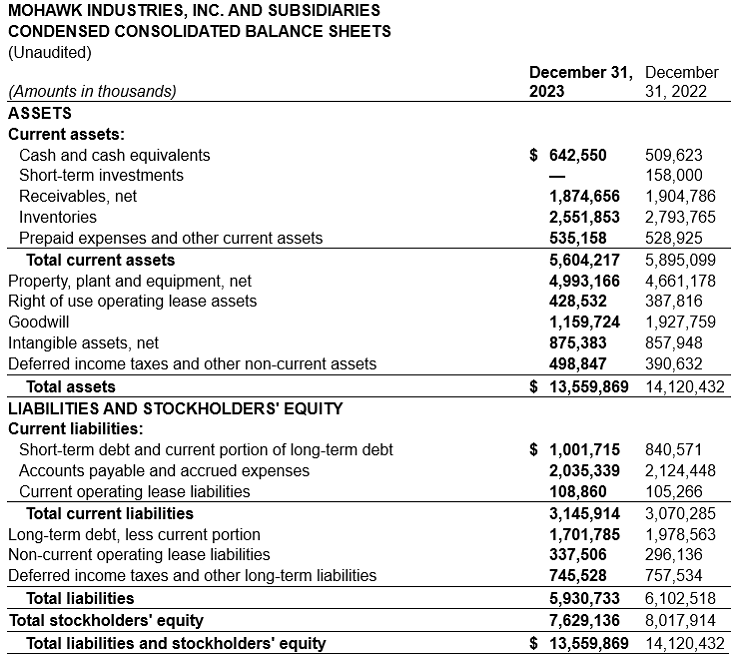

For the twelve months ending December 31, 2023, the Company reported a net loss of $440 million and a loss per share of $6.90, which included non-cash impairment charges of $878 million; adjusted net earnings were $587 million, and adjusted EPS was $9.19. For the 2023 twelve-month period, net sales were $11.1 billion, a decrease of 5.1% as reported and 7.7% on a legacy and constant basis versus the prior year. For the twelve-month period ending December 31, 2022, the Company reported net sales of $11.7 billion, net earnings of $25 million and EPS of $0.39; adjusted net earnings were $823 million, and adjusted EPS was $12.85.

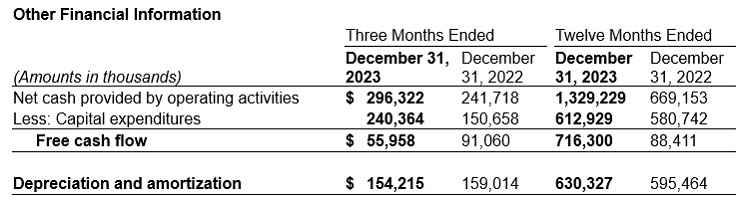

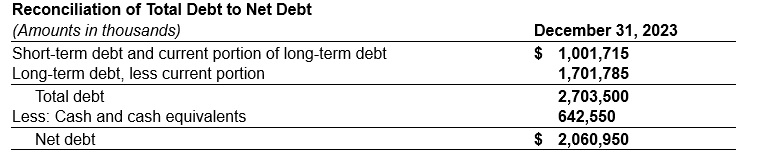

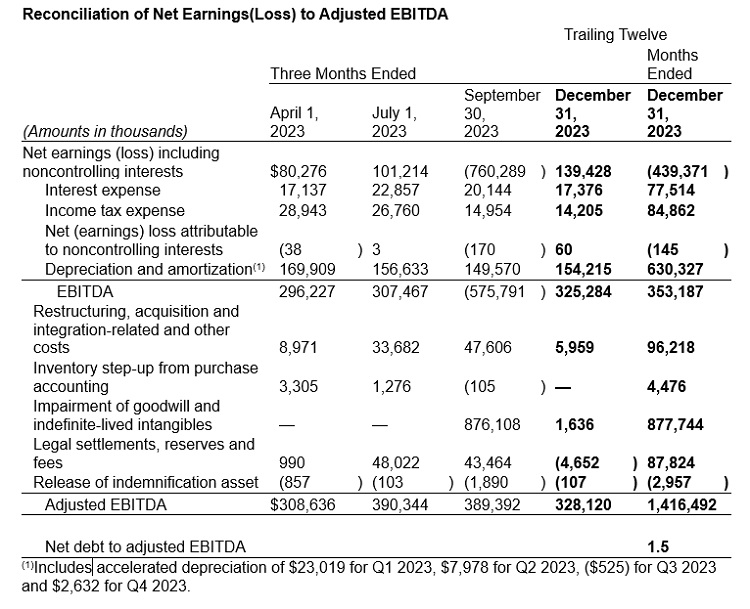

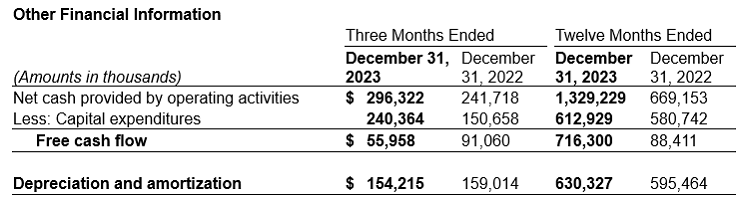

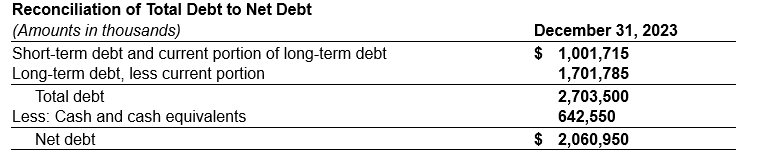

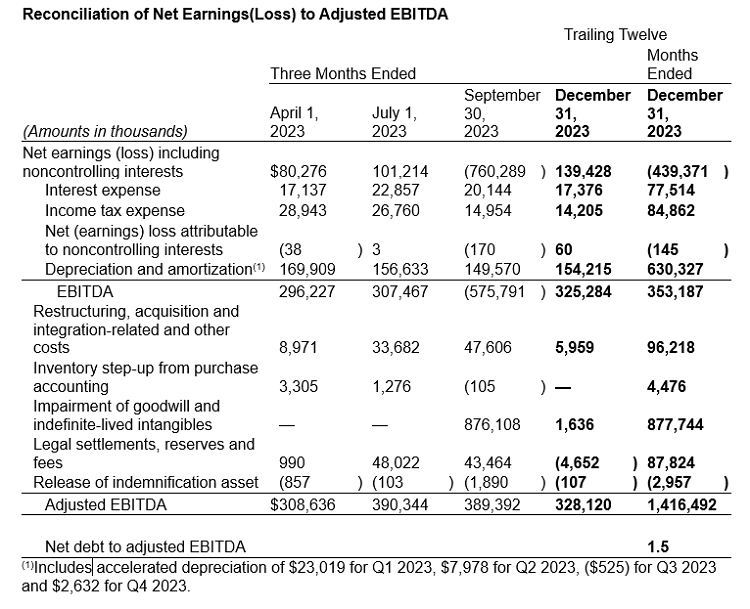

Commenting on the Company’s fourth quarter and full year results, Chairman and CEO Jeff Lorberbaum stated, “Our fourth quarter results were ahead of our expectations, with benefits from cost containment, productivity and lower input costs. The industry reduced selling prices and we passed through declining costs in energy and raw materials. Under these conditions, we focused on optimizing our revenues and reducing our costs through restructuring actions and manufacturing enhancements. We aggressively managed inventory levels, which reduced our working capital compared to prior year by more than $300 million, excluding acquisitions. We also have invested in sales resources, merchandising and new products with innovative features to inspire consumers to purchase flooring. We closed the year with a net debt to adjusted EBITDA ratio of 1.5 times, free cash flow of $716 million and available liquidity of $1.9 billion, and we are retiring a higher interest rate term loan of approximately $900 million in the first quarter of 2024. We are well positioned to manage current conditions and emerge stronger from this economic cycle when the rebound occurs.

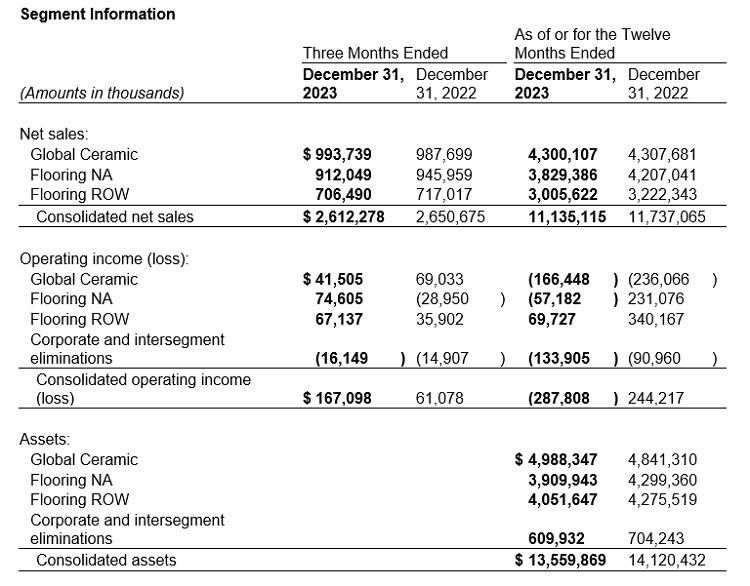

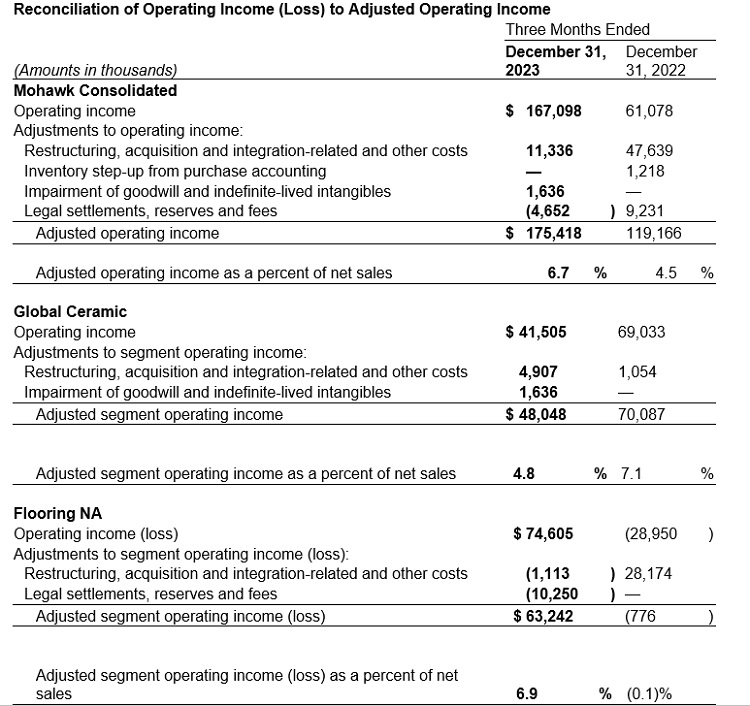

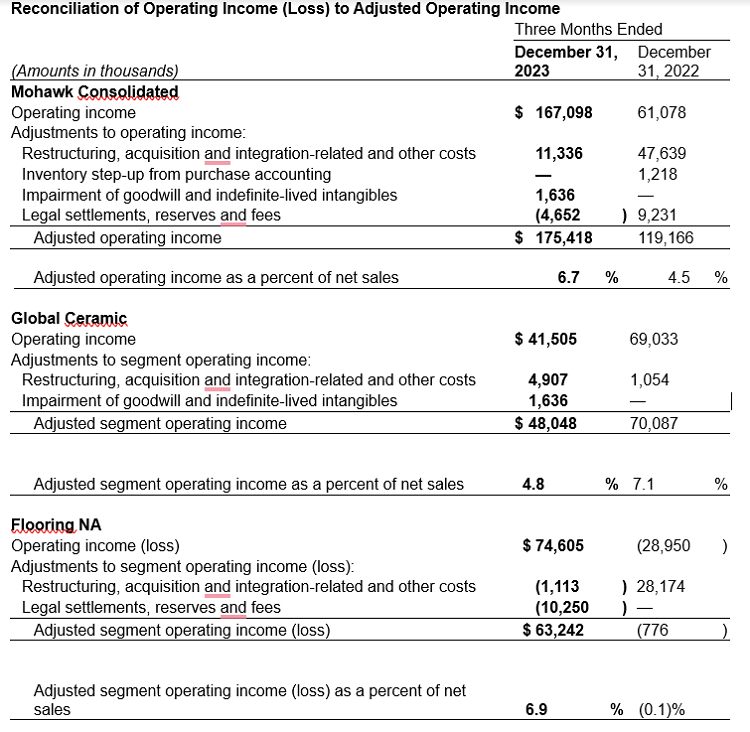

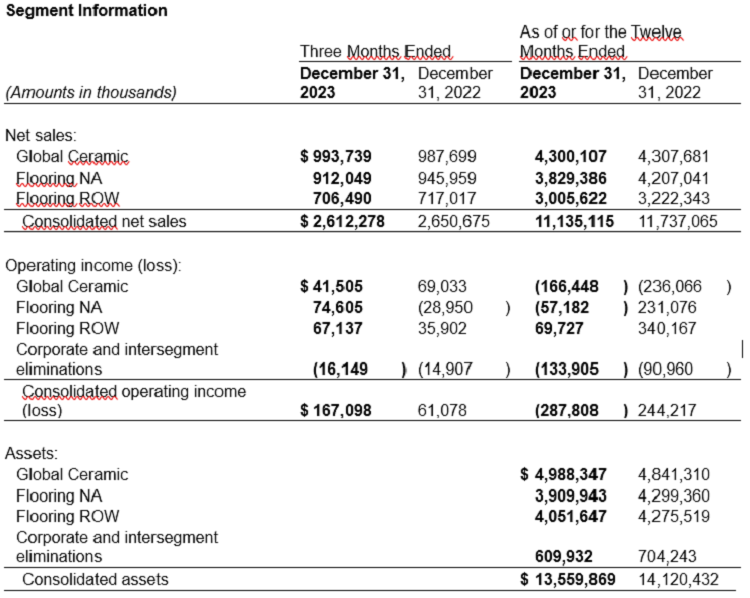

For the fourth quarter, the Global Ceramic Segment reported a 0.6% increase in net sales as reported, or a 4.7% decline on a legacy and constant basis. The Segment’s operating margin was 4.2% as reported, or 4.8% on an adjusted basis. Across the segment, we are managing production to align with demand and have significantly reduced inventory throughout the year. To contain costs, we have increased productivity, reduced overhead and implemented alternative formulations. In the U.S., we are expanding our distribution through our local service centers and offering new collections with premium Italian styling to improve our product mix. We have integrated Vitromex in Mexico and Elizabeth in Brazil and are enhancing our sales, marketing and operational strategies. In both countries, demand significantly declined last year due to rising interest rates and slowing economic conditions, which reduced our results. In Italy, we are optimizing our recent expansion of premium porcelain slabs to meet growing demand in both the residential and commercial channels.

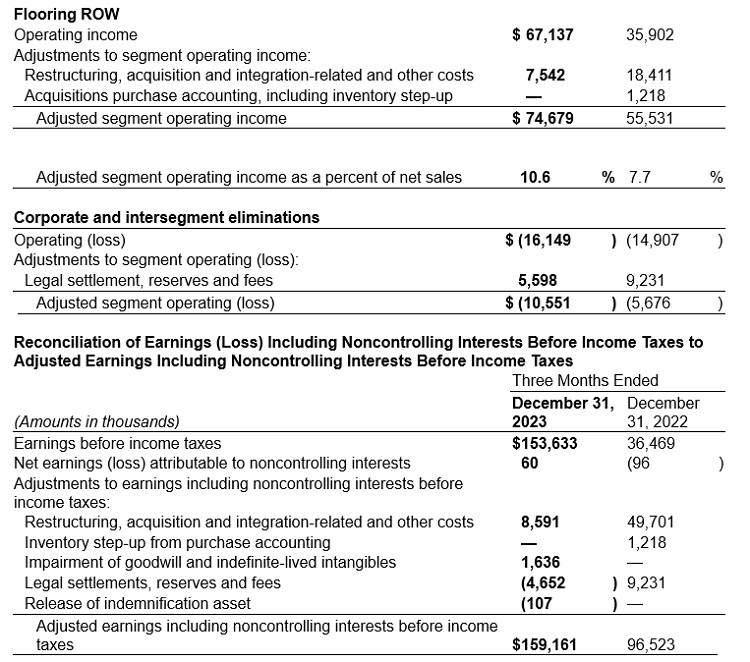

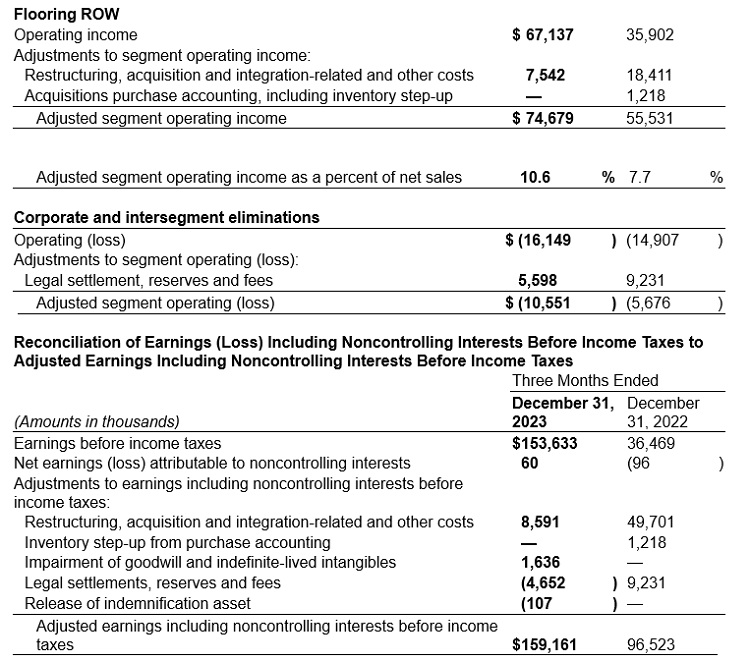

During the fourth quarter, our Flooring Rest of the World Segment’s net sales decreased by 1.5% as reported, or 4.1% on a legacy and constant currency basis. The Segment’s operating margin was 9.5% as reported, or 10.6% on an adjusted basis. The European building product category remains under stress, with consumers remaining cautious and retailers reducing their inventory levels. We are investing in new products for 2024 while implementing tight cost controls. We are re-energizing our flagship Quick-Step brand with inspirational interactive merchandising displays. We are completing the transition to rigid LVT, and we have decommissioned our residential flexible line. Our wood panels performance has declined during the year from cyclically high pricing to a more competitive environment with excess capacity. We continue to implement restructuring actions in the segment and enhance our recent smaller European bolt-on acquisitions, including insulation, MDF boards, sheet vinyl and mezzanine flooring.

In the fourth quarter, our Flooring North America Segment sales declined 3.6%. The Segment’s operating margin was 8.2% as reported, or 6.9% on an adjusted basis. Reduced market volumes led to low industry utilization rates and aggressive competition in the marketplace. We are continuing to invest in sales and marketing initiatives to expand our distribution and improve our long-term growth. To enhance our business, we are making capital investments to increase our differentiated features and lower our manufacturing costs. In each product category, we are introducing innovative new collections, which are being well accepted. The commercial channel outperformed our expectations, led by the hospitality sector. We are leveraging our customer relationships to expand our needle punch flooring and trim acquisitions.

As we enter 2024, our industry is at a cyclical low and we expect seasonality in the first quarter to be more aligned with long-term historical levels. Our businesses are minimizing expenses, reducing overhead and restructuring operations to adapt to present conditions. We are continuing to invest in innovative products to increase sales and mix. We are reacting to competitive pressures to optimize our volumes as we pass through declines in input costs. We continue to manage our inventory and anticipate temporary shutdowns to align with demand. All of our businesses are implementing process enhancement initiatives to reduce the impact of inflation. Given these factors, we anticipate our first quarter adjusted EPS to be between $1.60 and $1.70.

During the past eighteen months, we have initiated many actions across the company to improve our cost structure, manage lower volume and integrate our recent acquisitions. Combined with these actions, improving industry conditions as we emerge from the bottom of this cycle should improve our results in the second half of the year. Markets anticipate that central banks will lower interest rates, expanding home sales, residential remodeling and commercial projects. The pace of improvement of the flooring category will be dependent on inflation rates, consumer confidence and the strength of home sales. We believe the U.S. and Latin American markets could improve before Europe, which could lag due to current geopolitical pressures. After past housing recessions, our industry has rebounded with increased sales and expanding margins for multiple years. Housing remains in short supply across all our geographies, and increased remodeling investments will be required to update the aging housing stock. Our restructuring actions, investments in new technologies, targeted expansions and recent acquisitions will enable us to further expand our business. As the world’s largest flooring company, we believe we are uniquely positioned to improve our results as the market recovers.”

ABOUT MOHAWK INDUSTRIES

Mohawk Industries is the leading global flooring manufacturer that creates products to enhance residential and commercial spaces around the world. Mohawk’s vertically integrated manufacturing and distribution processes provide competitive advantages in the production of carpet, rugs, ceramic tile, laminate, wood, stone and vinyl flooring. Our industry leading innovation has yielded products and technologies that differentiate our brands in the marketplace and satisfy all remodeling and new construction requirements. Our brands are among the most recognized in the industry and include American Olean, Daltile, Durkan, Eliane, Elizabeth, Feltex, GH Commercial, Godfrey Hirst, Grupo Daltile, IVC Commercial, IVC Home, Karastan, Marazzi, Mohawk, Mohawk Group, Mohawk Home, Pergo, Quick-Step, Unilin and Vitromex. During the past decade, Mohawk has transformed its business from an American carpet manufacturer into the world’s largest flooring company with operations in Australia, Brazil, Canada, Europe, Malaysia, Mexico, New Zealand, Russia and the United States.

Certain of the statements in the immediately preceding paragraphs, particularly anticipating future performance, business prospects, growth and operating strategies and similar matters and those that include the words “could,” “should,” “believes,” “anticipates,” “expects,” and “estimates,” or similar expressions constitute “forward-looking statements.” For those statements, Mohawk claims the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995. There can be no assurance that the forward-looking statements will be accurate because they are based on many assumptions, which involve risks and uncertainties. The following important factors could cause future results to differ: changes in economic or industry conditions; competition; inflation and deflation in freight, raw material prices and other input costs; inflation and deflation in consumer markets; currency fluctuations; energy costs and supply; timing and level of capital expenditures; timing and implementation of price increases for the Company’s products; impairment charges; integration of acquisitions; international operations; introduction of new products; rationalization of operations; taxes and tax reform; product and other claims; litigation; geopolitical conflict; regulatory and political changes in the jurisdictions in which the Company does business; and other risks identified in Mohawk’s SEC reports and public announcements.

Conference call Friday, February 9, 2024, at 11:00 AM Eastern Time

To participate in the conference call via the Internet, please visit http://ir.mohawkind.com/events/event-details/mohawk-industries-inc-4th-quarter-2023-earnings-call. To participate in the conference call via telephone, register in advance at https://dpregister.com/sreg/10185489/fb57257e00 to receive a unique personal identification number or dial 1-833-630-1962 for U.S./Canada and 1-412-317-1843 for international/local on the day of the call for operator assistance. A replay will be available until March 8, 2024, by dialing 1-877-344-7529 for U.S./Canada calls and 1-412-317-0088 for international/local calls and entering access code #3161276.

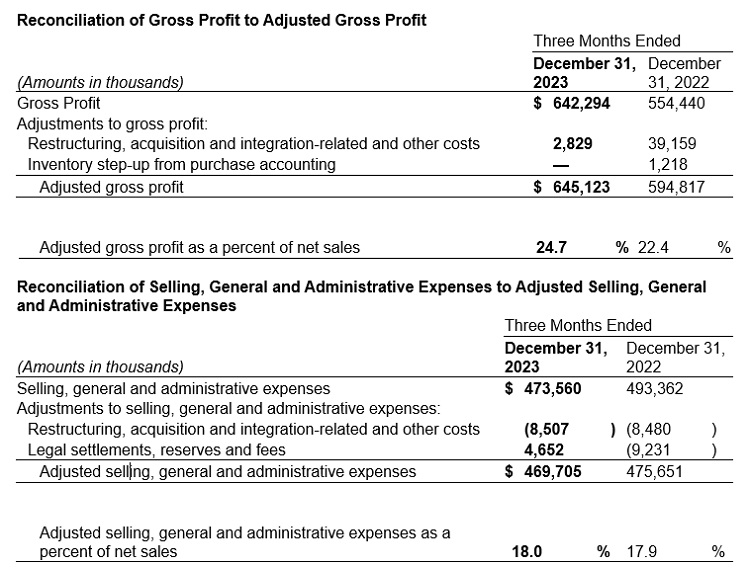

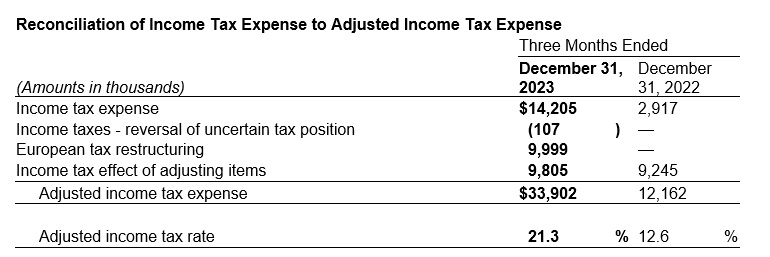

The Company supplements its condensed consolidated financial statements, which are prepared and presented in accordance with US GAAP, with certain non-GAAP financial measures. As required by the Securities and Exchange Commission rules, the tables above present a reconciliation of the Company’s non-GAAP financial measures to the most directly comparable US GAAP measure. Each of the non-GAAP measures set forth above should be considered in addition to the comparable US GAAP measure, and may not be comparable to similarly titled measures reported by other companies. The Company believes these non-GAAP measures, when reconciled to the corresponding US GAAP measure, help its investors as follows: Non-GAAP revenue measures that assist in identifying growth trends and in comparisons of revenue with prior and future periods and non-GAAP profitability measures that assist in understanding the long-term profitability trends of the Company's business and in comparisons of its profits with prior and future periods.

The Company excludes certain items from its non-GAAP revenue measures because these items can vary dramatically between periods and can obscure underlying business trends. Items excluded from the Company’s non-GAAP revenue measures include: foreign currency transactions and translation; more or fewer shipping days in a period and the impact of acquisitions.

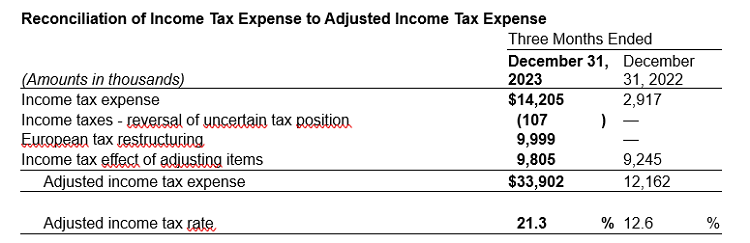

The Company excludes certain items from its non-GAAP profitability measures because these items may not be indicative of, or are unrelated to, the Company's core operating performance. Items excluded from the Company's non-GAAP profitability measures include: restructuring, acquisition and integration-related and other costs, legal settlements, reserves and fees, impairment of goodwill and indefinite-lived intangibles, acquisition purchase accounting, including inventory step-up from purchase accounting, release of indemnification assets, the reversal of uncertain tax positions and European tax restructuring.

KONTAKT:

James Brunk, Chief Financial Officer

tel.: (706) 624-2239

Źródło informacji: GlobeNewswire

| Data publikacji | 09.02.2024, 12:56 |

| Źródło informacji | GlobeNewswire |

| Zastrzeżenie | Za materiał opublikowany w serwisie PAP MediaRoom odpowiedzialność ponosi – z zastrzeżeniem postanowień art. 42 ust. 2 ustawy prawo prasowe – jego nadawca, wskazany każdorazowo jako „źródło informacji”. Informacje podpisane źródłem „PAP MediaRoom” są opracowywane przez dziennikarzy PAP we współpracy z firmami lub instytucjami – w ramach umów na obsługę medialną. Wszystkie materiały opublikowane w serwisie PAP MediaRoom mogą być bezpłatnie wykorzystywane przez media. |

Newsletter portalu PAP MediaRoom to przesyłane do odbiorców raz dziennie zestawienie informacji prasowych, komunikatów instytucji oraz artykułów dziennikarskich, które zostały opublikowane na portalu danego dnia.

ZAPISZ SIĘ

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}