Mohawk Industries Reports Q1 Results

28.04.2023, 10:29aktualizacja: 28.04.2023, 10:40

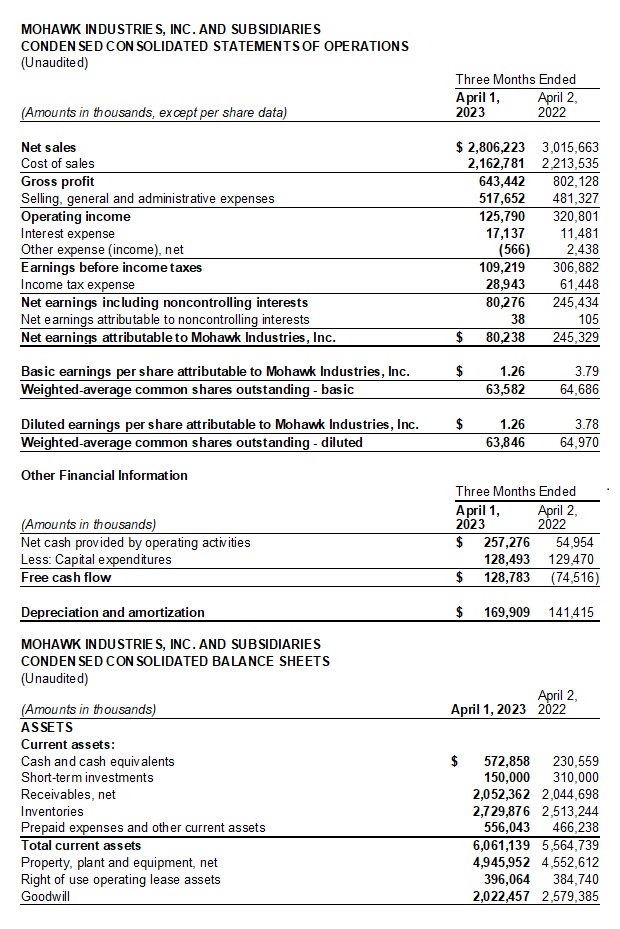

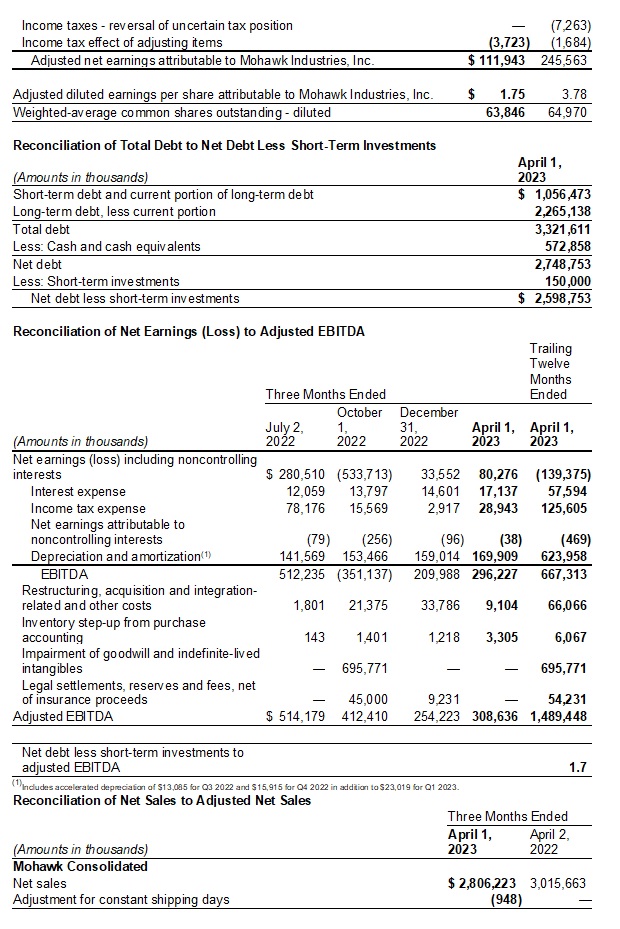

CALHOUN, Ga., April 27, 2023 (GLOBE NEWSWIRE) -- Mohawk Industries, Inc. (NYSE: MHK) today announced first quarter 2023 net earnings of $80 million and diluted earnings per share (EPS) of $1.26. Adjusted net earnings were $112 million, and adjusted EPS was $1.75, excluding restructuring, acquisition and other charges. Net sales for the first quarter of 2023 were $2.8 billion, a decrease of 6.9% as reported and 5.9% on a constant currency and days basis. For the first quarter of 2022, net sales were $3.0 billion, net earnings were $245 million and EPS was $3.78. Adjusted net earnings were $246 million, and adjusted EPS was $3.78, excluding restructuring, acquisition and other charges.

Commenting on Mohawk Industries’ first quarter performance, Jeffrey S. Lorberbaum, Chairman and CEO, stated, “All of our businesses are adapting our strategies to a more challenging environment. We are managing our costs while investing in both our short and long-term growth. We exceeded our earnings expectations with the business maintaining higher pricing and stronger mix, and Flooring Rest of the World outperforming the other segments. The commercial channel continued to be stronger than residential with home remodeling projects being postponed and new housing construction being impacted by higher mortgage rates. Our balance sheet remains strong, and we generated $129 million of free cash flow in the quarter.”

We strategically invested in new product innovation, enhanced merchandising and customer trade shows to improve sales. We are continuing to reduce costs across the enterprise by enhancing productivity, streamlining processes and controlling administrative expenses. Our customers remained conservative with their inventory commitments, and our operations are running at lower utilization levels, creating higher costs from unabsorbed overhead. In Flooring North America and Flooring Rest of the World, our restructuring actions are on track and should improve the results of our business.

We are limiting our capital investments to those providing significant sales, margin and process improvements. We are expanding our constrained categories that have the greatest growth potential when the economy improves, including LVT, premium laminate, quartz countertops, porcelain slabs and insulation products. We completed two ceramic acquisitions in Brazil and Mexico that had combined sales of approximately $425 million in 2022, almost doubling our existing market share. We are developing strategies to increase sales and beginning to consolidate the businesses to reduce cost, improve efficiencies and optimize production. We also continue to improve the small bolt-on acquisitions in Europe and the U.S. that we completed last year.

Natural gas and electricity inflation remained a headwind in the first quarter, though our future results will benefit as lower energy costs flow through our P&L. Our sustainability strategy includes investments in the production of green energy, which reduces both our expenses and carbon footprint. Our two biomass energy plants lowered our costs and improved our results in the quarter. We also purchased some of our European energy at various times to reduce future cost volatility. Italian energy subsidies have recently been extended at reduced levels through the second quarter of 2023.

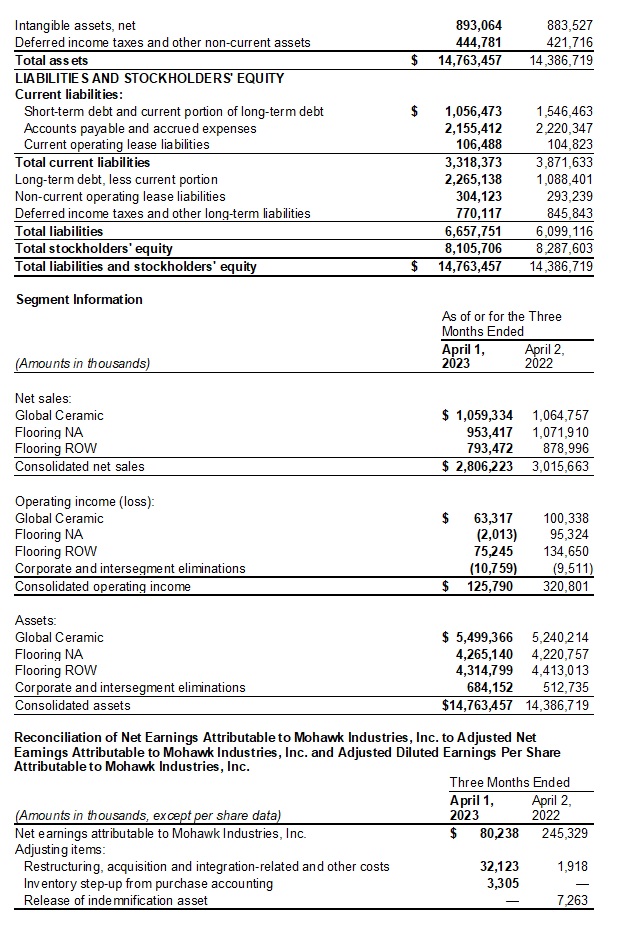

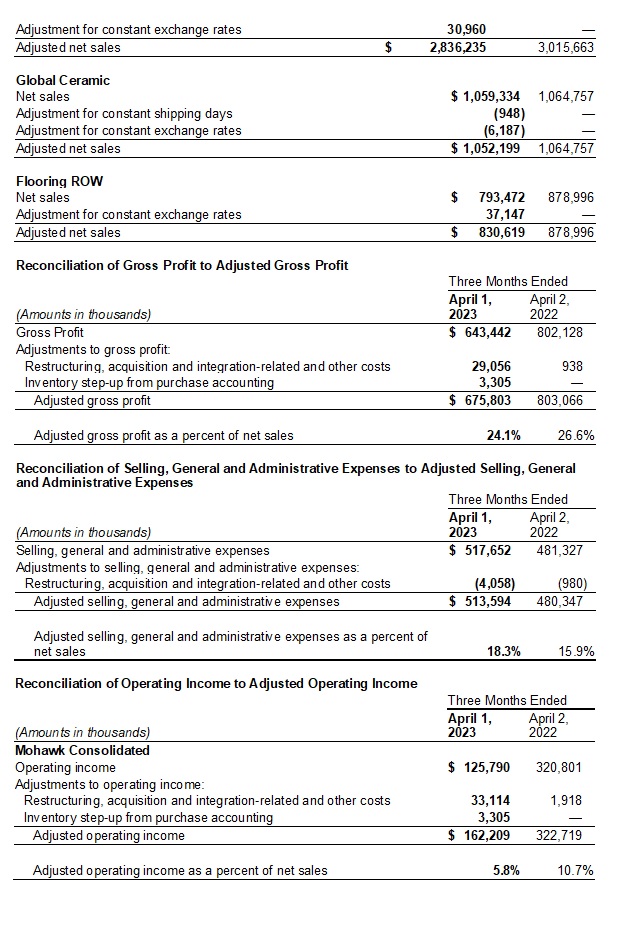

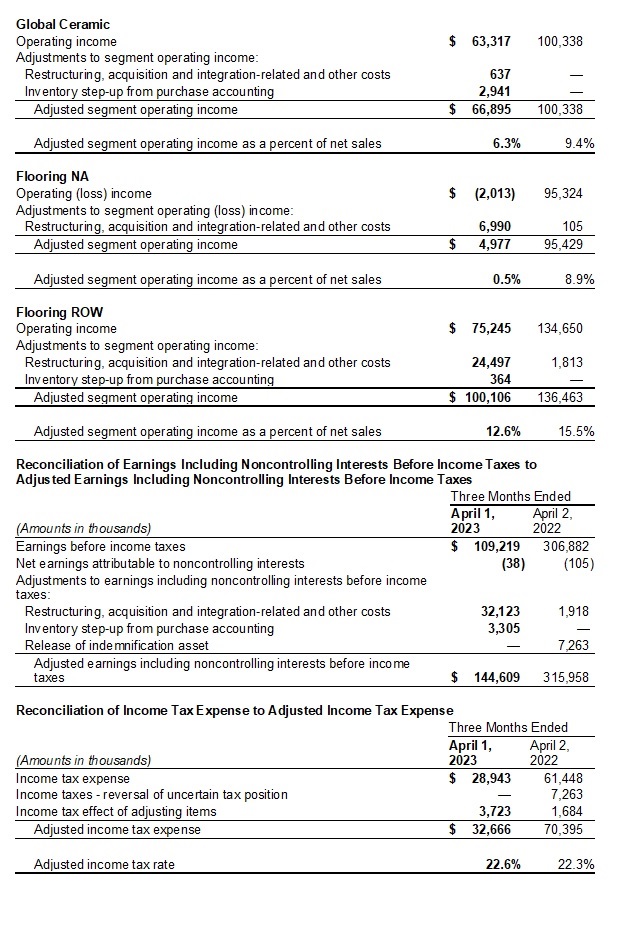

For the first quarter, the Global Ceramic Segment reported a 0.5% decline in net sales as reported, or a 1.2% decline on a constant currency and days basis. The Segment’s operating margin was 6.0% as reported, or 6.3% on an adjusted basis, as a result of favorable pricing and product mix and productivity gains, offset by inflation, lower volumes and temporary shutdowns. Our 2023 product launches with new sizes, unique visuals and polished finishes are benefiting our mix. We are reducing production to align with demand and competition in the marketplace is increasing. The U.S. is performing better than our other ceramic markets due to our greater sales in the commercial sector. Our more reliable U.S. domestic production is benefiting our sales, particularly in our premium collections that provide alternatives to European products. To increase our quartz countertop volume, we are expanding our business with national accounts, contractors and kitchen and bath retailers. In our European ceramic business, we maintained higher average selling prices than we anticipated, though our volumes decreased as residential remodeling slowed. Our other ceramic markets also declined with reduced spending on homes and greater reductions in customer inventories, though our sales trends in these regions seasonally improved as we progressed through the period.

During the first quarter, our Flooring Rest of the World Segment’s net sales decreased by 9.7% as reported or 5.5% on a constant currency and days basis. The Segment’s operating margin was 9.5% as reported, or 12.6% on an adjusted basis, as a result of favorable pricing and product mix offset by inflation, lower volumes and temporary shutdowns. Our European businesses have been compressed as high energy prices and inflation impacted consumer budgets. Compared to the prior quarter, the Segment's business improved as we increased promotions to strengthen sales, had fewer shutdowns, lowered costs and expanded product options for more constrained consumer budgets. As input costs decline, we expect competitive pressures to increase in the market. Both laminate and LVT volumes were lower in the quarter, and we are controlling our costs and production levels in response. We have begun the conversion of our residential LVT from flexible to rigid and are preparing to restructure the operations. Our sheet vinyl volume increased as consumers sought options to lower remodeling costs. In our new Eastern European sheet vinyl acquisition, we are improving the product offering and enhancing the facility’s production and efficiencies. Our panels business has slowed with the market and inventory reductions in the channel. Our margins were higher than anticipated due to stronger pricing, lower input costs and benefits from our biomass energy production. We are making progress on achieving planned synergies in our French panels and German mezzanine flooring acquisitions. Our insulation category performed the best in the Segment as energy efficiency has become a greater priority, and our polyurethane products provide the greatest heat resistant properties. We have integrated our insulation acquisition in Ireland and the U.K., and our new facility is ramping up production ahead of schedule. In Australia and New Zealand, our results were reduced by higher interest rates and lower volumes. We are selectively introducing promotions to drive sales and have raised prices to offset cost inflation.

In the first quarter, our Flooring North America Segment sales decreased 11.1%. The Segment had a negative operating margin of 0.2% as reported, or positive 0.5% on an adjusted basis, as a result of favorable pricing and product mix along with productivity gains, offset by inflation, reduced volumes, temporary shutdowns and incremental marketing investments. The Segment has been challenged by significant inflation, higher interest rates and more restrictive lending, which have weakened the housing market and our industry. As a result, our customers are more tightly managing their inventory levels, and we are aligning production with demand. Our margins should expand in the second quarter as our input costs improve and plant utilization increases. Our restructuring actions are on track and will lower our cost in the residential and commercial soft surface categories. Commercial sales remained solid with new construction and remodeling projects continuing in most channels. The commercial flooring accessories acquisition we completed last year has complemented our product offering and benefited our business. Sales of residential soft surfaces declined more than our other categories. The multifamily business remains the strongest category in residential, and we are expanding our participation in the channel. The U.S. LVT market is becoming more competitive as the industry slows and ocean freight costs decline. Imports from Asia are being interrupted as the U.S. requires proof of supply chain compliance as part of the forced labor protection act. Our West Coast LVT plant is continuing to ramp up and production will increase as we move through the year. Sheet vinyl sales are outperforming as consumers seek more budget-oriented options. During the quarter, our laminate sales in retail expanded with its increased acceptance as a waterproof alternative, though volumes in the other channels declined.

Our industry is operating in a completely different environment than a year ago. Around the world, central banks are raising interest rates to slow their economies and reduce inflation. These actions lower our industry volume as new home sales and residential remodeling are postponed. The commercial sector has remained stronger than residential, though higher interest rates and tighter lending requirements could affect business investments as the year progresses. We are maximizing our sales and distribution by focusing on better performing channels, introducing differentiated products and providing enhanced service and value. We are proactively managing our spending and cost structures to optimize our results. We anticipate that industry volume and pricing will remain under pressure across our markets. We expect seasonal improvement in demand along with reduced energy and material costs to improve our future results. Given these factors, we anticipate our second quarter adjusted EPS to be between $2.56 and $2.66, excluding any restructuring, acquisition and other charges.

This industry downturn is unique, with employment remaining high, businesses continuing to invest and homes maintaining their valuations. We are conservatively managing the near term while we invest in long-term growth through product innovation, capacity expansions and acquisitions. Our strong balance sheet enables us to navigate the current downturn as we prepare for the industry rebound that follows. Longer term, all of our regions require the updating of aging houses and significant new home construction to satisfy market needs. With our strength across regions, markets and products, we anticipate capturing increased opportunities when the recovery occurs in the housing market and the economy.

ABOUT MOHAWK INDUSTRIES

Mohawk Industries is the leading global flooring manufacturer that creates products to enhance residential and commercial spaces around the world. Mohawk’s vertically integrated manufacturing and distribution processes provide competitive advantages in the production of carpet, rugs, ceramic tile, laminate, wood, stone and vinyl flooring. Our industry leading innovation has yielded products and technologies that differentiate our brands in the marketplace and satisfy all remodeling and new construction requirements. Our brands are among the most recognized in the industry and include American Olean, Daltile, Durkan, Eliane, Feltex, Godfrey Hirst, IVC, Karastan, Marazzi, Mohawk, Mohawk Group, Pergo, Quick-Step and Unilin. During the past decade, Mohawk has transformed its business from an American carpet manufacturer into the world’s largest flooring company with operations in Australia, Brazil, Canada, Europe, Malaysia, Mexico, New Zealand, Russia and the United States.

Certain of the statements in the immediately preceding paragraphs, particularly anticipating future performance, business prospects, growth and operating strategies and similar matters and those that include the words “could,” “should,” “believes,” “anticipates,” “expects,” and “estimates,” or similar expressions constitute “forward-looking statements.” For those statements, Mohawk claims the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995. There can be no assurance that the forward-looking statements will be accurate because they are based on many assumptions, which involve risks and uncertainties. The following important factors could cause future results to differ: changes in economic or industry conditions; competition; inflation and deflation in freight, raw material prices and other input costs; inflation and deflation in consumer markets; currency fluctuations; energy costs and supply; timing and level of capital expenditures; timing and implementation of price increases for the Company’s products; impairment charges; integration of acquisitions; international operations; introduction of new products; rationalization of operations; taxes and tax reform; product and other claims; litigation; the risks and uncertainty related to the COVID-19 pandemic; regulatory and political changes in the jurisdictions in which the Company does business; and other risks identified in Mohawk’s SEC reports and public announcements.

Conference call Friday, April 28, 2023, at 11:00 AM Eastern Time

To participate in the conference call via the Internet, please visit http://ir.mohawkind.com/events/event-details/mohawk-industries-inc-1st-quarter-2023-earnings-call. To participate in the conference call via telephone, register in advance at https://dpregister.com/sreg/10177490/f8f85704c6 to receive a unique personal identification number or dial 1-833-630-1962 for U.S./Canada and 1-412-317-1843 for international/local on the day of the call for operator assistance. A replay will be available until May 26, 2023, by dialing 1-877-344-7529 for U.S./Canada calls and 1-412-317-0088 for international/local calls and entering access code #6741654.

The Company supplements its condensed consolidated financial statements, which are prepared and presented in accordance with US GAAP, with certain non-GAAP financial measures. As required by the Securities and Exchange Commission rules, the tables above present a reconciliation of the Company’s non-GAAP financial measures to the most directly comparable US GAAP measure. Each of the non-GAAP measures set forth above should be considered in addition to the comparable US GAAP measure, and may not be comparable to similarly titled measures reported by other companies. The Company believes these non-GAAP measures, when reconciled to the corresponding US GAAP measure, help its investors as follows: Non-GAAP revenue measures that assist in identifying growth trends and in comparisons of revenue with prior and future periods and non-GAAP profitability measures that assist in understanding the long-term profitability trends of the Company's business and in comparisons of its profits with prior and future periods.

The Company excludes certain items from its non-GAAP revenue measures because these items can vary dramatically between periods and can obscure underlying business trends. Items excluded from the Company’s non-GAAP revenue measures include: foreign currency transactions and translation.

The Company excludes certain items from its non-GAAP profitability measures because these items may not be indicative of, or are unrelated to, the Company's core operating performance. Items excluded from the Company's non-GAAP profitability measures include: restructuring, acquisition and integration-related and other costs, legal settlements, reserves and fees, net of insurance proceeds, impairment of goodwill and indefinite-lived intangibles, acquisition purchase accounting, including inventory step-up from purchase accounting, release of indemnification assets and the reversal of uncertain tax positions.

CONTACT:

James Brunk

Chief Financial Officer

tel. (706) 624-2239

Źródło informacji: GlobeNewswire

| Data publikacji | 28.04.2023, 10:29 |

| Źródło informacji | GlobeNewswire |

| Zastrzeżenie | Za materiał opublikowany w serwisie PAP MediaRoom odpowiedzialność ponosi – z zastrzeżeniem postanowień art. 42 ust. 2 ustawy prawo prasowe – jego nadawca, wskazany każdorazowo jako „źródło informacji”. Informacje podpisane źródłem „PAP MediaRoom” są opracowywane przez dziennikarzy PAP we współpracy z firmami lub instytucjami – w ramach umów na obsługę medialną. Wszystkie materiały opublikowane w serwisie PAP MediaRoom mogą być bezpłatnie wykorzystywane przez media. |

Newsletter portalu PAP MediaRoom to przesyłane do odbiorców raz dziennie zestawienie informacji prasowych, komunikatów instytucji oraz artykułów dziennikarskich, które zostały opublikowane na portalu danego dnia.

ZAPISZ SIĘ