Mohawk Industries Reports Q1 Results

05.05.2020, 12:13aktualizacja: 05.05.2020, 12:13

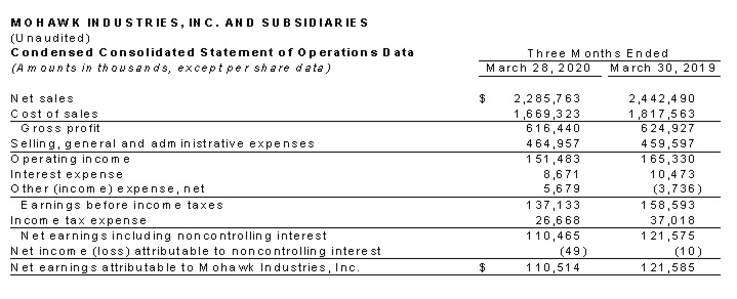

CALHOUN, Ga., May 04, 2020 (GLOBE NEWSWIRE) -- Mohawk Industries, Inc. (NYSE: MHK) today announced 2020 first quarter net earnings of $111 million and diluted earnings per share (EPS) of $1.54. Adjusted net earnings were $119 million, and EPS was $1.66, excluding restructuring, acquisition and other charges. Net sales for the first quarter of 2020 were $2.3 billion, down 6.4% as reported and 3.5% on a constant currency and days basis. For the first quarter of 2019, net sales were $2.4 billion, net earnings were $122 million and EPS was $1.67, adjusted net earnings were $154 million, and EPS was $2.13, excluding restructuring, acquisition and other charges.

Commenting on Mohawk Industries’ first quarter performance, Jeffrey S. Lorberbaum, Chairman and CEO, stated, “The world changed during the first quarter, and we are now managing through an unprecedented situation. Mohawk entered the year as the world’s leading flooring company with a strong presence in all product categories, manufacturing in 18 countries and sales in more than 170 nations. During 2019, we generated $1.4 billion of operating cash flow, and we have a strong balance sheet and leverage of 1.6x, near our historical low. We recently obtained a $500 million term loan to expand our liquidity to $1.3 billion after we pay off a €300 million note this month. With no other maturities in 2020, we have liquidity to manage through the downturn and strengthen our position when the economy recovers. We are reducing capital expenditures, cutting non-essential expenses and putting our stock purchases on hold until the environment improves.”

Until the COVID-19 outbreak, our results for the quarter were in line with our plan, as we benefited from the initiatives we implemented in 2019. As we progressed through the period, government actions to reduce the spread of the virus impacted all our markets, with some shutting down retail and manufacturing operations. Across all of our markets, demand has dropped dramatically, with residential remodeling being impacted the most up to this point and DIY products performing best, as some people started projects while staying home.

To respond to this global event, we have established corporate, segment and business teams to manage our actions as conditions change. We are keeping employees safe, increasing work from home and adjusting strategies as required. As demand dropped, we significantly reduced production, and are making weekly adjustments to adapt to the changing environment. Even where mandatory shutdowns were initiated, we are shipping product from inventory to our customers that are operating. We are lowering our costs by implementing layoffs and furloughs, using government assistance where available and absorbing labor costs where mandated to do so. We are benefiting from lower raw material and energy costs, though other headwinds are considerably greater. We are limiting our expenses and investments to what is essential to run the business and enhancing reports to manage major areas of focus, including inventory levels, headcount, receivables and payables.

Each of our segments and individual businesses has strong leaders that have managed through difficult circumstances multiple times during their careers. Our entire global team is taking extraordinary steps to support our customers and protect our people and business. Our organization is flexible in adapting to fluid conditions, and we are applying the lessons we learned from 9/11 and the last recession to guide us through these times.

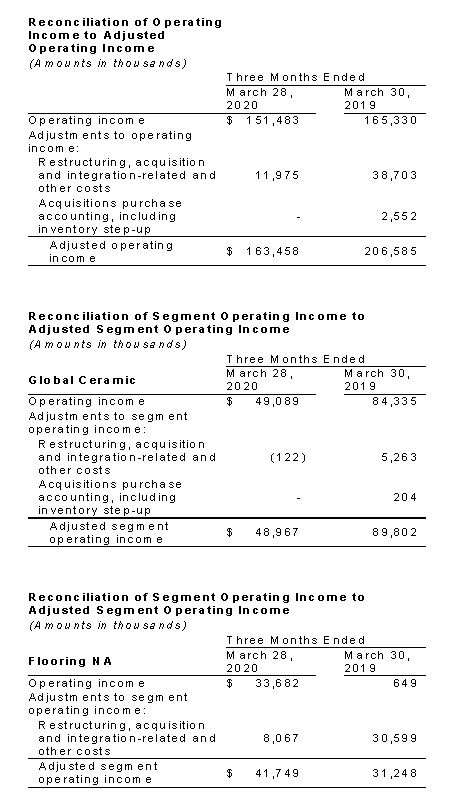

For the quarter, our Global Ceramic Segment sales declined 6% as reported and 2% on a constant currency and days basis. The segment’s operating margin was 6% as reported, declining year over year primarily due to lower volume, unfavorable price and mix and unplanned shutdown costs due to COVID-19, partially offset by productivity and lower start-up cost. Each of the segment’s regions was affected by the virus at different points in the period, with Italy at the forefront. In each region, we are lowering our production with demand, reducing our cost structure and adapting to different government programs in each country. Our U.S. ceramic business has a higher percentage of new residential and commercial sales, so demand has declined more slowly as those projects are still being completed. Through February, U.S. ceramic imports were 18% lower than the prior year, and average import pricing rose 5%. Our click ceramic production continues to ramp up as we begin introducing new collections into different channels. We are increasing our higher value quartz countertops as our productivity and cost continue to improve. In Mexico, our first quarter sales were slightly better than last year, with our mix declining due to increased competition, higher inflation and investments to expand commercial distribution. Though the Mexican government shut down manufacturing in April, we continued to ship from inventory. In Brazil, our results were good, even though the virus negatively impacted the end of the period. Our European ceramic business was on plan until the outbreak stopped production, and shipments to customers have continued. In our Russian business, our volume was stronger than expected due to customers increasing their inventory levels, anticipating higher inflation. Much of Russia is now locked down, with many stores and construction sites closed.

During the quarter, our Flooring North America Segment’s sales decreased 8% as reported and approximately 5.5% with one less day and the exit of unprofitable wood and other products with an operating margin of 4% as reported and 5% excluding restructuring and other charges. Operating income for the segment increased primarily due to improvements in productivity and reductions in inflation, partially offset by lower volume, price, mix and COVID-19. Across the business, we are reducing production and implementing layoffs and furloughs to align with the abrupt decline in demand. The segment has a higher percentage of sales from remodeling, and a large number of our retailers are not operating. Many retailers that carry our rug collections have also been closed. Our carpet sales performed best in the builder, multi-family, education and government sectors as projects underway have continued. During the quarter, LVT and sheet vinyl performed the best in the segment. Our LVT operations have improved with higher daily output and increased uptime. To improve our margins and mix, we have introduced collections featuring enhanced design and performance under our premium brands. Like resilient flooring, our state-of-the-art laminate also provides a DIY alternative with realistic visuals, water-proof technology and enhanced durability. In our wood flooring business, we have restructured our manufacturing operations and increased productivity and yields, improving our margins.

For the quarter, our Flooring Rest of the World Segment’s sales decreased 5% as reported and were flat on a constant currency and days basis. The segment’s operating margin was 13% as reported and 14% excluding restructuring and other charges due to lower price and mix, volume and shutdown costs from COVID-19, partially offset by lower inflation and increased productivity. Across our product categories, we have continued shipping from inventory to support customers that are operating. During the first quarter, the product categories in which we have made recent investments, including rigid LVT, sheet vinyl and carpet tile, delivered growth in a difficult environment. LVT outperformed as it takes market share from other product categories. Our sheet vinyl business grew due to exports outside the region, and higher sales in Russia, where our new plant is operating well. As we exited the quarter, our laminate volume declined with the rest of the business, primarily in countries most impacted by the outbreak. We completed the closure of our wood flooring plant in the Czech Republic, which will reduce costs in our Malaysian operation as it reopens from a mandatory shutdown. Our insulation plants in France and Ireland have ceased manufacturing, and our other plants are reducing production and placing workers on temporary unemployment. Our board operations are being impacted similarly to the rest of the business, and we are starting and stopping production with temporary layoffs. In Australia and New Zealand, our sales were up slightly with hard surfaces growing and lower carpet sales pressuring margins. A major update of many of our product lines is being well accepted. In late March, New Zealand’s government enacted a stringent lockdown, shuttering our operations and retail outlets throughout April.

As we enter May, the coronavirus is dramatically disrupting the economies around the world. Some countries are beginning to explore easing restrictions, while others are extending them. Presently, all our plants around the world are in operation except those in Mexico and a small plant in Pennsylvania. We are focused on conserving cash, adjusting production, reducing inventory and preserving our operational capabilities. We are also reducing expenses and investments and aligning with government requirements and support. The rate at which governments will open commerce and the subsequent consumer response cannot be determined. Some businesses have postponed investments in both remodeling and new construction until a recovery becomes more apparent. At the end of April, with most people sheltering in place across the world, our sales rate is about 35% below the prior year, and we cannot predict the pace at which it will recover. Given these circumstances, we are unable to provide EPS guidance for the second quarter, and we anticipate an operating loss in the period due to the impact of COVID-19. Our balance sheet is strong with substantial liquidity of $1.3 billion to manage through this crisis. Our business model remains solid with strong local teams in each market taking the necessary actions to manage the downturn. The economies will return to normal over time, and we are optimistic about the long-term future of our business.

About Mohawk Industries

Mohawk Industries is the leading global flooring manufacturer that creates products to enhance residential and commercial spaces around the world. Mohawk’s vertically integrated manufacturing and distribution processes provide competitive advantages in the production of carpet, rugs, ceramic tile, laminate, wood, stone and vinyl flooring. Our industry leading innovation has yielded products and technologies that differentiate our brands in the marketplace and satisfy all remodeling and new construction requirements. Our brands are among the most recognized in the industry and include American Olean, Daltile, Durkan, Eliane, Feltex, Godfrey Hirst, IVC, Karastan, Marazzi, Mohawk, Mohawk Group, Pergo, Quick-Step and Unilin. During the past decade, Mohawk has transformed its business from an American carpet manufacturer into the world’s largest flooring company with operations in Australia, Brazil, Canada, Europe, India, Malaysia, Mexico, New Zealand, Russia and the United States.

Certain of the statements in the immediately preceding paragraphs, particularly anticipating future performance, business prospects, growth and operating strategies and similar matters and those that include the words “could,” “should,” “believes,” “anticipates,” “expects,” and “estimates,” or similar expressions constitute “forward-looking statements.” For those statements, Mohawk claims the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995. There can be no assurance that the forward-looking statements will be accurate because they are based on many assumptions, which involve risks and uncertainties. The following important factors could cause future results to differ: changes in economic or industry conditions; competition; inflation and deflation in raw material prices and other input costs; inflation and deflation in consumer markets; energy costs and supply; timing and level of capital expenditures; timing and implementation of price increases for the Company’s products; impairment charges; integration of acquisitions; international operations; introduction of new products; rationalization of operations; taxes and tax reform, product and other claims; litigation; the risks and uncertainty related to the COVID-19 pandemic; and other risks identified in Mohawk’s SEC reports and public announcements.

Conference call Tuesday, May 5, 2020, at 11:00 AM Eastern TimeThe telephone number is 1-800-603-9255 for US/Canada and 1-706-634-2294 for International/Local. Conference ID # 5997678. A replay will be available until June 5, 2020, by dialing 1-855-859-2056 for US/local calls and 1-404-537-3406 for International/Local calls and entering Conference ID # 5997678.

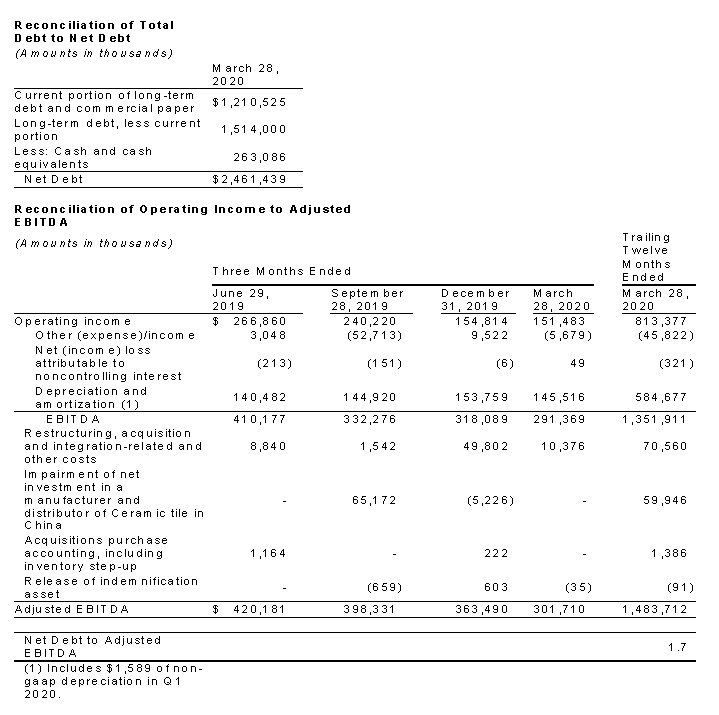

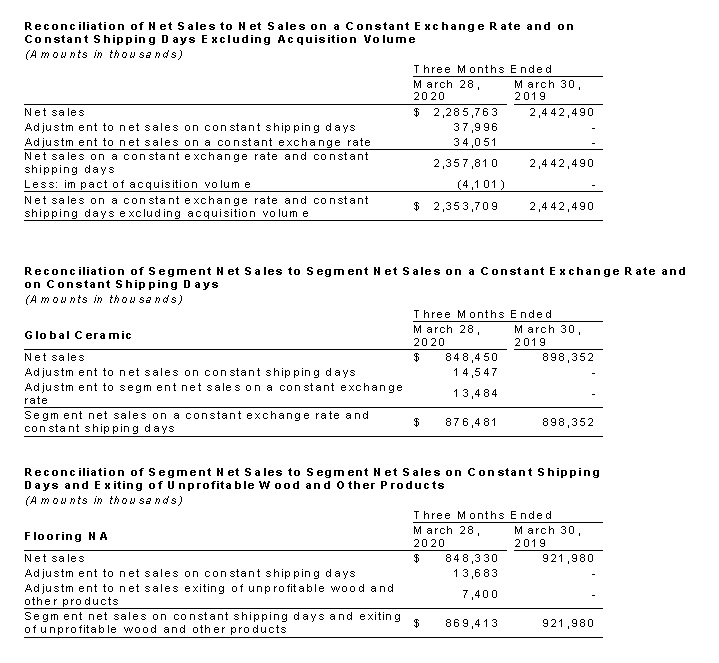

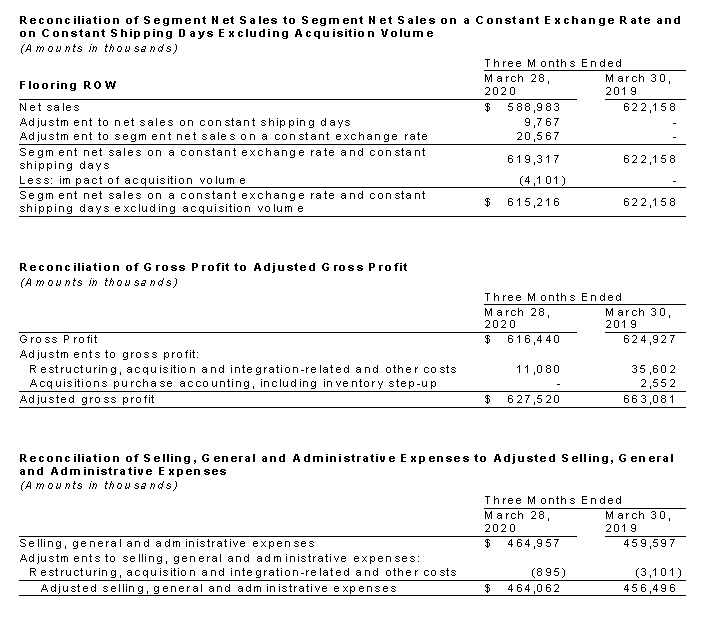

The Company supplements its condensed consolidated financial statements, which are prepared and presented in accordance with US GAAP, with certain non-GAAP financial measures. As required by the Securities and Exchange Commission rules, the tables above present a reconciliation of the Company's non-GAAP financial measures to the most directly comparable US GAAP measure. Each of the non-GAAP measures set forth above should be considered in addition to the comparable US GAAP measure, and may not be comparable to similarly titled measures reported by other companies. The Company believes these non-GAAP measures, when reconciled to the corresponding US GAAP measure, help its investors as follows: Non-GAAP revenue measures that assist in identifying growth trends and in comparisons of revenue with prior and future periods and non-GAAP profitability measures that assist in understanding the long-term profitability trends of the Company's business and in comparisons of its profits with prior and future periods.

The Company excludes certain items from its non-GAAP revenue measures because these items can vary dramatically between periods and can obscure underlying business trends. Items excluded from the Company's non-GAAP revenue measures include: foreign currency transactions and translation and the impact of acquisitions.

The Company excludes certain items from its non-GAAP profitability measures because these items may not be indicative of, or are unrelated to, the Company's core operating performance. Items excluded from the Company's non-GAAP profitability measures include: restructuring, acquisition and integration-related and other costs, acquisition purchase accounting, including inventory step-up, release of indemnification assets and the reversal of uncertain tax positions.

CONTACT:

Frank Boykin

Chief Financial Officer

tel. (706) 624-2695

| Data publikacji | 05.05.2020, 12:13 |

| Źródło informacji | GlobeNewswire |

| Zastrzeżenie | Za materiał opublikowany w serwisie PAP MediaRoom odpowiedzialność ponosi – z zastrzeżeniem postanowień art. 42 ust. 2 ustawy prawo prasowe – jego nadawca, wskazany każdorazowo jako „źródło informacji”. Informacje podpisane źródłem „PAP MediaRoom” są opracowywane przez dziennikarzy PAP we współpracy z firmami lub instytucjami – w ramach umów na obsługę medialną. Wszystkie materiały opublikowane w serwisie PAP MediaRoom mogą być bezpłatnie wykorzystywane przez media. |

Newsletter portalu PAP MediaRoom to przesyłane do odbiorców raz dziennie zestawienie informacji prasowych, komunikatów instytucji oraz artykułów dziennikarskich, które zostały opublikowane na portalu danego dnia.

ZAPISZ SIĘ