Clean energy technology supply chains must get better, faster, cleaner

09.06.2023, 09:38aktualizacja: 09.06.2023, 09:47

LONDON, June 08, 2023 (GLOBE NEWSWIRE) -- Rapidly scaling sustainable, diversified, and resilient clean energy supply chains is key to achieving net-zero targets on-time and at as low a cost as possible, according to the ETC. Its latest insights briefing, „Better, Faster, Cleaner: Securing clean energy technology supply chains”, highlights that global supply of key materials and components is sufficient to meet growing demand for clean energy technologies (wind, solar, batteries, grids, heat pumps) over the medium- to long-term. However, in the short- to medium-term, policy and industry action is critical to overcome supply chain challenges that put the energy transition at risk.

Clean energy supply chain challenges

The global transition to net-zero demands a massive increase in clean energy technology. Clean electrification is the backbone of the transition to net-zero and will provide over 60% of all energy consumed in 2050, up from 20% today. [1] Achieving this would need wind and solar capacity to increase 2.5-4 times and electric vehicle (EV) sales will need to grow over sixfold by 2030 from current levels. While it is fundamentally possible to deliver the transition at cost by mid-century, three key supply-side challenges must be addressed in the short- to medium-term:

These challenges can be addressed by strong regulation and industry action, but might also entail cost trade-offs if near-shoring is also prioritised. For example, the estimated costs of building solar PV manufacturing capacity (from polysilicon through to modules) are currently almost 4 times higher in the EU and the US than in China. [2] Other considerations include balancing political priorities, such as creating local jobs and energy security, with feasibility challenges, for example, caused by stringent environmental and social standards, slow permitting, and difficulties in accessing finance.

„The energy transition is fundamentally achievable if supply chain risks are managed. In addressing these challenges, there are some clear wins to pursue and some trickier trade-offs which require deep thought from governments and industry. The priority should be to rapidly scale and diversify supply chains to build resilient clean energy capacity while localising manufacturing where there is a clear competitive advantage and alignment with domestic priorities” - says Adair Turner, Chair of the Energy Transitions Commission.

Immediate policy and industry action are key to progress the energy transition at the speed and scale required to meet net-zero targets by 2050.

„The supply chains covered in this report are critical to the energy transition. Key factors for reliability, risk, and stability are brought to the forefront, while bottlenecks and key actions inform for a more rapid and just transition” - said Jean-Pascal Tricoire, Chairman of Schneider Electric.

Key areas of particular short-term concern are:

Critical areas of action for governments & policymakers and industry

„Our decarbonization targets imply a transition from an >>expenditure<< economy based on fossil fuels to an >>investment<< economy in clean energies. Materials and component supplies will be increasingly important. Industry has the ability and the will to scale-up their activities, although policy action is needed now to ensure the production of materials and components can increase to the levels needed and to reinforce the global supply chains. Innovation and international collaboration will also be key to achieve material efficiency and recycling of used products” - said Agustín Delgado, Chief Innovation and Sustainability Officer at Iberdrola.

Energy security as a global priority

The Covid-19 pandemic, volatile commodity and shipping costs, the Russian invasion of Ukraine and the ensuing European energy crisis resulted in delays and price increases that shocked global supply chains. This led governments around the world to realise the importance of energy security, reassess domestic policies and invest more in clean energy. Most notable was the passage of the US „Inflation Reduction Act” in 2022 and the EU „Green Deal Industrial Plan”, announced in response.

The ETC’s accompanying „EU Policy Toolkit” proposes action for EU policymakers to address Europe’s vulnerability to supply chain shocks, given its high dependence on imports for key raw materials (copper, lithium, nickel and cobalt in particular) and components for clean energy technology. It builds on existing EU regulations and recommendations from the Insights Briefing.

„The latest ETC Insights Briefing highlights that we have the critical minerals needed to support the transition to clean energy, and can innovate to address critical supply chain bottlenecks created by market tightness, environmental and social concerns, and concentration of production. We should be optimistic that solutions are already emerging from research and development, process efficiency, community engagement, and material recycling that will pull this future closer. The clean energy manufacturing market represents a compelling opportunity for private and public sectors around the world” - said Jon Creyts, CEO of RMI.

„Better, Faster, Cleaner: Securing clean energy technology supply chains” has been developed in collaboration with the European Climate Foundation and ETC members from across industry, financial institutions and environmental advocacy including Arcelor Mittal, Bank of America, BP, EBRD, HSBC, Iberdrola, Impax, Legal and General, National Grid, Ørsted, Rio Tinto, Schneider Electric, Royal Dutch Shell, Tata Group, Volvo Group, the World Resources Institute and Worley.

This report constitutes a collective view of the Energy Transitions Commission. Members of the ETC endorse the general thrust of the arguments made in this report but should not be taken as agreeing with every finding or recommendation. The institutions with which the Commissioners are affiliated have not been asked to formally endorse the report.

To read the full report, visit: https://www.energy-transitions.org/publications/better-faster-cleaner-supply-chains/.

Notes to editors

[1] ETC (2021), „Making Clean Electrification Possible”.

[2] BNEF (2022), „Building solar factories to rival China won’t be cheap”.

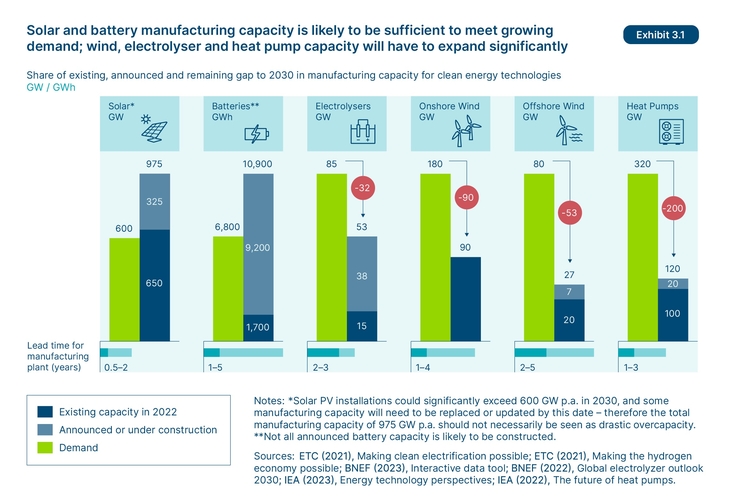

Solar and battery manufacturing capacity is likely to be sufficient to meet growing demand; however, wind, electrolyser and heat pump capacity will have to expand significantly. This is shown in the exhibit accompanying this announcement, available at https://www.globenewswire.com/NewsRoom/AttachmentNg/a0e6eaea-fc73-47b6-be8e-95aea46fa06b.

CONTACT:

Caroline Randle

Energy Transitions Commission

e-mail: caroline.randle@systemiq.earth

-

Susan Brownlow

e-mail: susan.brownlow@wordsforindustrypr.com

Source: GlobeNewswire

| Data publikacji | 09.06.2023, 09:38 |

| Źródło informacji | GlobeNewswire |

| Zastrzeżenie | Za materiał opublikowany w serwisie PAP MediaRoom odpowiedzialność ponosi – z zastrzeżeniem postanowień art. 42 ust. 2 ustawy prawo prasowe – jego nadawca, wskazany każdorazowo jako „źródło informacji”. Informacje podpisane źródłem „PAP MediaRoom” są opracowywane przez dziennikarzy PAP we współpracy z firmami lub instytucjami – w ramach umów na obsługę medialną. Wszystkie materiały opublikowane w serwisie PAP MediaRoom mogą być bezpłatnie wykorzystywane przez media. |

Newsletter portalu PAP MediaRoom to przesyłane do odbiorców raz dziennie zestawienie informacji prasowych, komunikatów instytucji oraz artykułów dziennikarskich, które zostały opublikowane na portalu danego dnia.

ZAPISZ SIĘ